December 06, 2023

Weekly Market Outlook

November 2023 surpassed all expectations in the stock and bond markets. Those investors who participated hit the bullseye. The month started off with a cooling CPI and PPI along with GDP jumping and the Fed’s hawkish stance softening. This was the exact recipe for lower interest rates, a weakening dollar, and risk-on assets beginning to recover and rally, producing a month of stock market returns that was one for the record books.

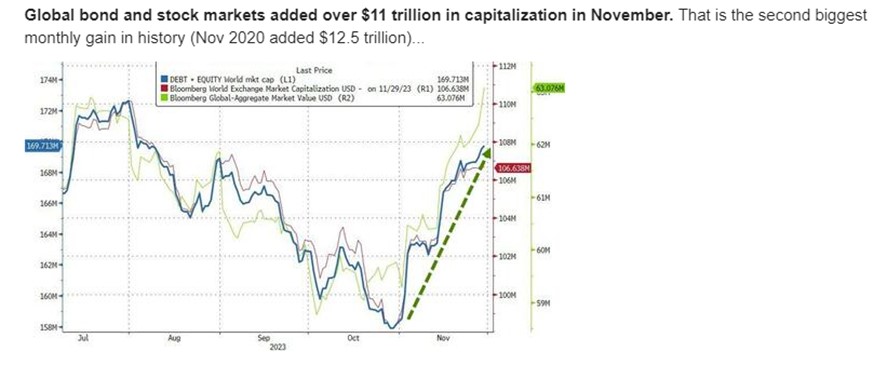

The S&P 500 was up 8.9% in November, the Barclays Aggregate Bond Fund (AGG core bonds) was up over 4%, and Corporate Bonds (LQD) were up over 7%. All impressive returns. Global assets had a huge increase in value and bonds had the best month in 40 years. See chart below:

Gaugers (and other friends), welcome to this week’s Market Outlook. We want to look at November and then bring an additional perspective of how far we have come, especially the past two years since the Fed began its unrelenting campaign of raising rates to cool the economy. Their hawkish posture was to contain the dreaded high inflation everyone in the US was feeling (and around the world as well).

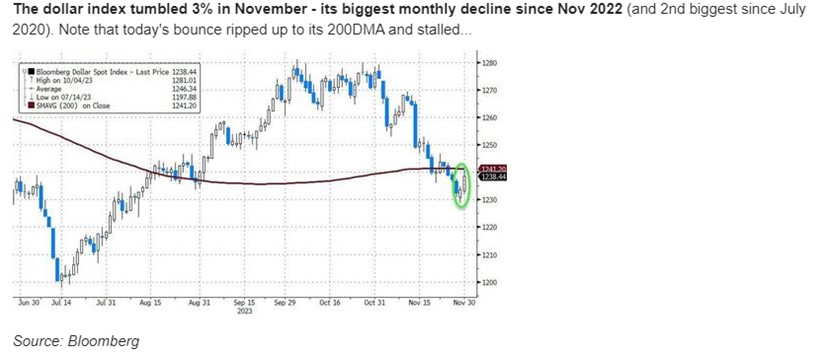

Interest rates coming down from 5% on the 10-year Treasury Bond along with a weakening US Dollar began the move into “risk assets” (i.e., the stock market).

We offer the following charts to illustrate some of the shifts in investor sentiment over the past 30 days:

The rally in bonds loosened financial conditions dramatically. See below:

The 20-year bond ETF, TLT, now sits at resistance. Which way will it go?

Bearish investor sentiment shifted quickly. See chart below:

Recent investor sentiment data supports that the bears have retrenched. See below:

At the end of November, the NASDAQ 100 (QQQ) erased the downward move that occurred over the past few months. See chart below:

And fueled a monumental move in the large-cap indices as we illustrate below:

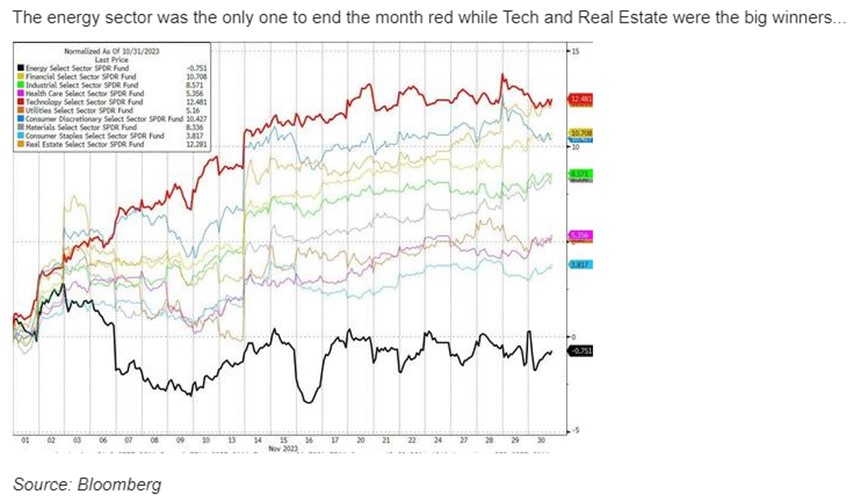

November saw an appreciation of every sector but Energy for the month. See chart below:

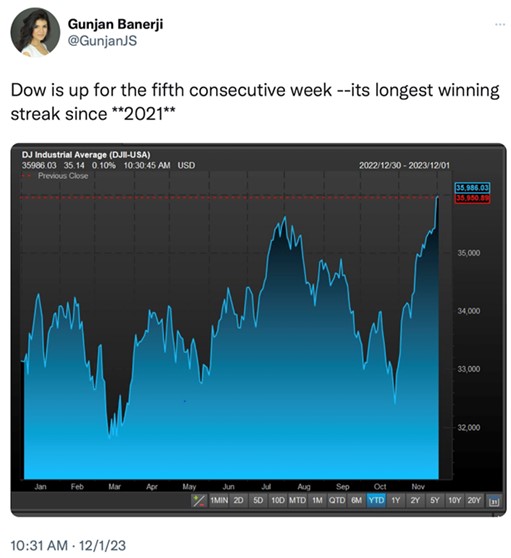

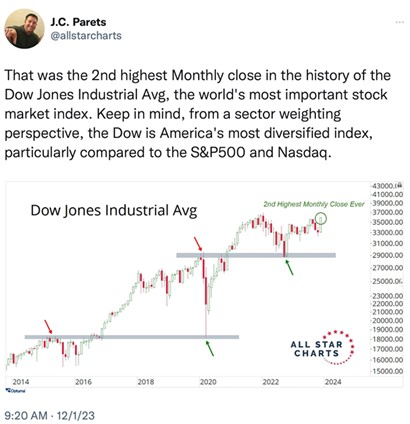

This past week saw the Dow Jones Industrial Average take the leadership role. As it hit a new 52 week. Also, the Dow is now up 5 straight weeks. See multiple Dow Jones charts below:

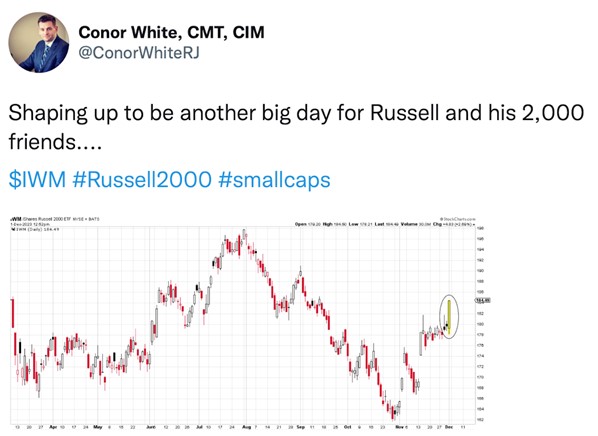

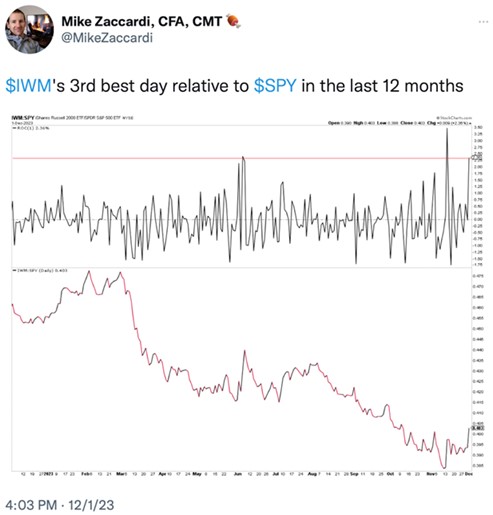

We also saw money rotate into more speculative areas of the market including small-caps, small technology companies and yesterday (Dec 1) small-cap value was the big winner. See charts below:

Last week we provided our own proprietary color charts showing the Dow, the S&P 500, and the NDX (NASDAQ 100) and why it confirmed our belief that the market was in a solid uptrend. If you would like to review these charts again (or did not see them), click here for a copy of last week’s Market Outlook.

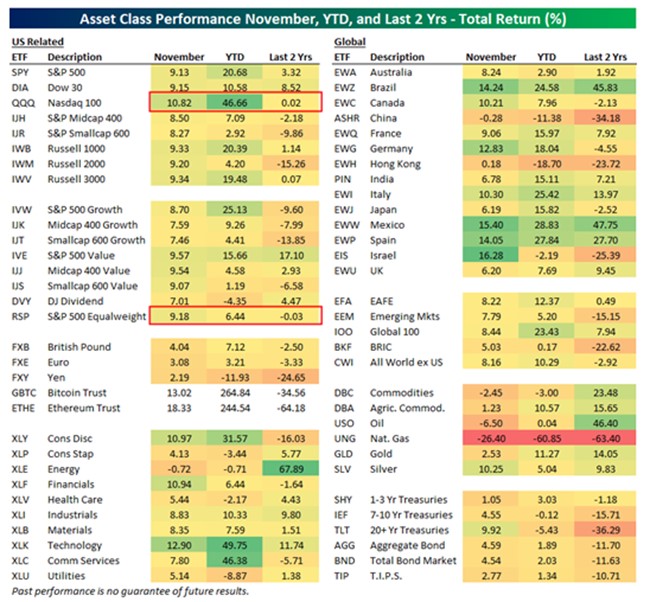

How did the big move up in November contribute to asset class and sector performance over the past two years?

Remember that most of the stock and bond indices went way down during 2022. Therefore, we were interested in where asset class performance stands for the past 2 years. You may be surprised to learn that the S&P 500 and the NASDAQ 100 (QQQ) are only just now breaking even from early 2022 index prices.

A full and detailed explanation of all asset class performance for the past 2 years is below. (While technology has come back strong, you might be surprised to learn that the S&P 500 Value and Energy have been the best two areas of the US markets for the past two years).

If you would like a similar comparison for the MarketGauge Pro investment strategies and S.M.A.R.T. All-Weather Portfolio Blends, please reach out to Rob or Benny as referenced at the end of this Market Outlook. It may surprise you to see how much better than the indices most of our investment strategies performed. And they did so with far less risk.

{kind=link}