Welcome back loyal readers to the weekly Market Outlook. We hope you had a good week, albeit a turbulent and difficult week for investors in the market.

The surprising (and unexpected) headline Wednesday morning on the CPI (Consumer Price Index) released at 8:30 a.m. EST, came in at 3.5% for March, significantly higher than February’s 3.2% (which was higher than expected in February).

This shocked the stock and bond markets and indicated that inflation is proving “stickier” than the Fed would like.

The market was down over 1% on Wednesday for most indices (down over 2% on small-cap stocks). However, a meaningful rally on Thursday recovered most of that down move from the day before.

On Friday morning, the PPI came out much more tame (good news). However, headlines regarding bank earnings, tensions in the Mideast, higher than expected interest rates, and negative earnings expectations heavily driven by JP Morgan’s earnings conference call spooked the market yet again. The markets gave up all of Thursday’s gains plus some.

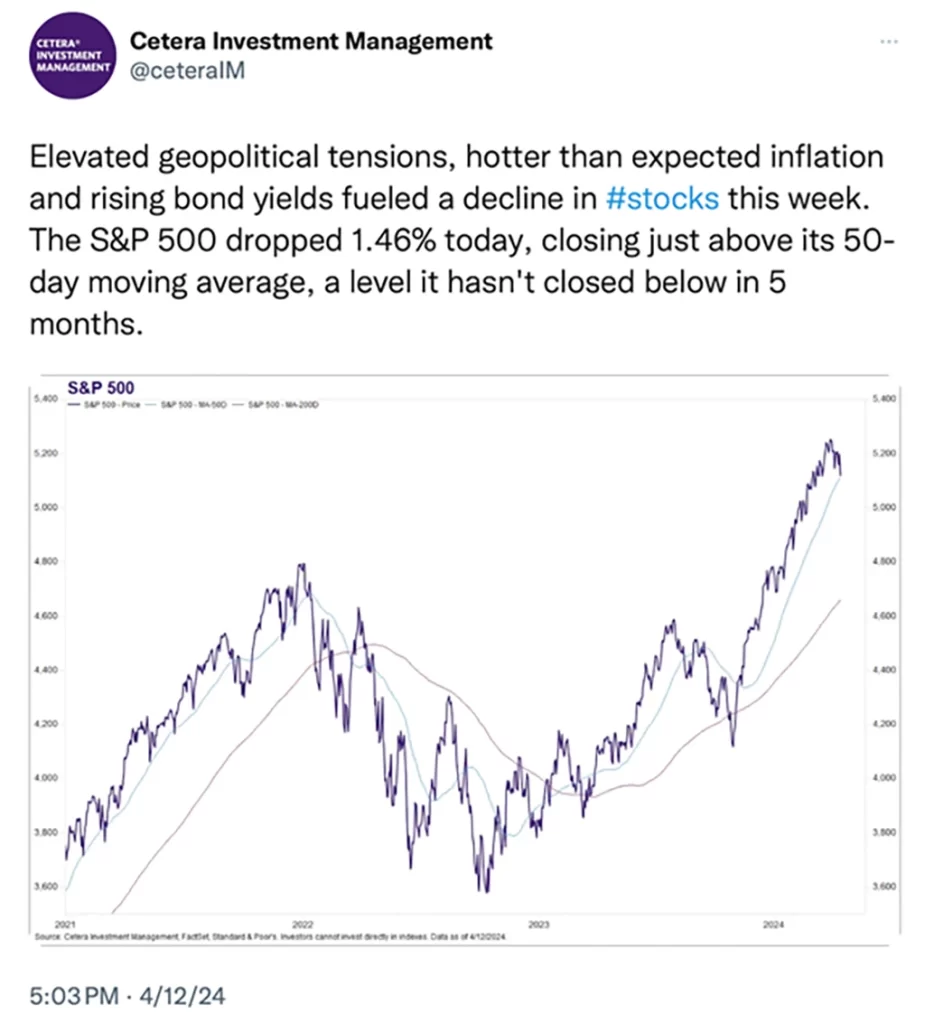

For the week, the S&P was down -1.5%, the NASDAQ 100 was only down 0.50%, but small-cap stocks (IWM) sank the most at -2.8%. That makes sense, given the much greater dependence that smaller companies have on interest rates. See chart below:

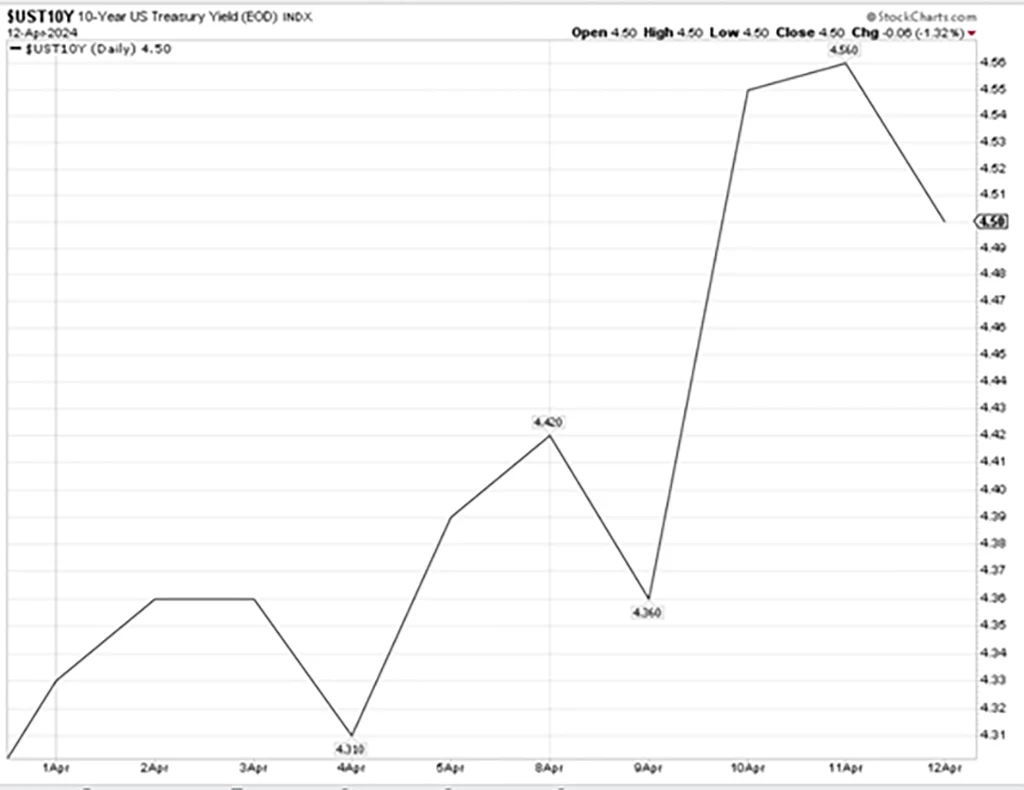

Fixed income funds and anything related to interest rates (small & midcap stocks) were most effected this past week. We wanted to illustrate just how quickly the 10-year interest rates reacted to the higher CPI number that came out. We illustrate this in the two charts below. The first is the most recent action since April 1 and the second is the rise in interest rates since January 1, 2024.

Since April 1, 2024, the 10-year interest rate has increased 5%. See below:

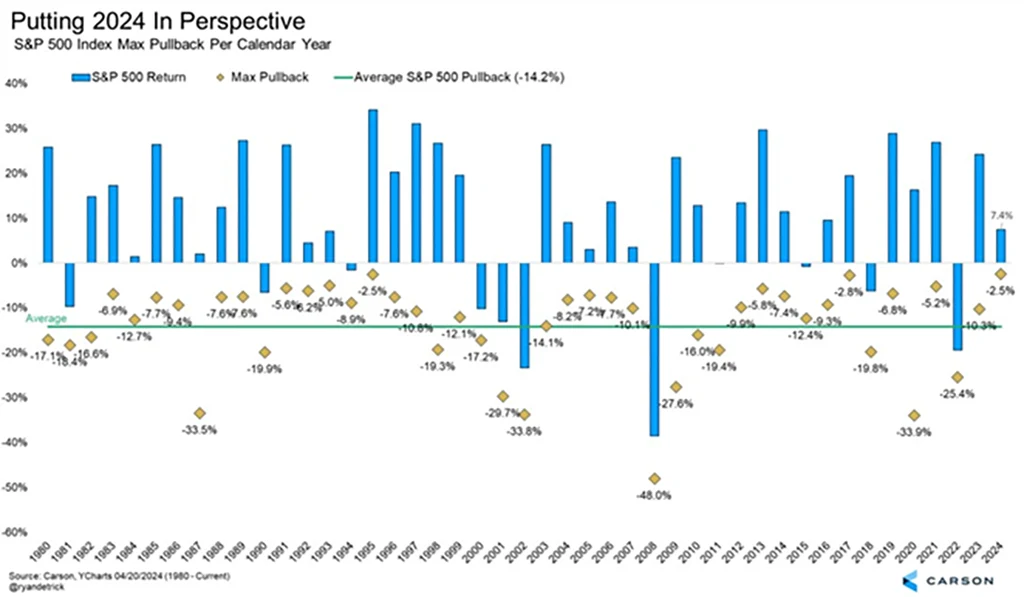

In the grand scheme of things, we are still close to new all-time highs set by the S&P 500 on March 28, 2024. Since then, we have seen a pick up in volatility and the daily market swings, but we are only down -2.3% since hitting the last all-time highs on March 28, 2024. Putting this in perspective is Ryan Detrick’s chart below:

Are we in for more downside? We will explore this shortly.

Who are you to believe?

There is a ton of news out there daily with contrarian points of view about our economy, inflation, debt, the markets, geopolitical risks, and an additional handful of potentially market moving data. Then there is what the Fed says.

Between Mish’s daily (you should be a subscriber and if you are not, why not? Go here to sign up for her daily musings and this weekly Market Outlook, as well as our vital BIG VIEW tools, you should have all you need to make intelligent investment decisions.

Add to that our easy to navigate, consistent outperforming investment strategies (with risk management) and you are well prepared to maneuver these markets and game plan for what might occur if we get into more difficult market conditions.

Starting late last year both Mish and I were redundant in our calls for “Higher for Longer” with respect to interest rates as well as inflation. We both repeated this mantra over and over. Mish was very clear when she laid out her projected path that historically inflation is stickier than investors are expecting. Inflation doesn’t just disappear overnight. Additionally, with all of the Government spending continuing, there is still an abundance of quantitative lubricant in the economy that will show up as inflationary.

Going back to the fall of 2023, we indicated that inflation was around for a much longer time than the deceleration that the analysts and pundits were projecting. Moreover, both in late 2023 and early 2024 we suggested that our opinion is that interest rate cuts would come later in 2024 and not be anywhere close to 6-7 times.

Since the beginning of the year, we were unequivocal in our belief that interest rate cuts wouldn’t happen until after midyear. The last two weeks (you can access the Market Outlook for the past two weeks here) we suggested that we were likely to see 3 or less interest rate cuts, if any.

Bloomberg reported on Saturday that there are now two new possibilities for the global inflation fight. First, the European Central Bank (ECB) may attempt something that diverges from the US. They are suggesting they will cut in June “even if the US holds fast”. “It’s time to diverge,” Bank of Greece Governor Yannis Stournaras said. “The situation in the euro area and the US are completely different.”

The other possibility? Brace yourself, said Bloomberg. If US inflation remains sticky, the Federal Reserve might do more than simply push back rate cuts. How about another rate hike? Bloomberg pointed out that robust consumption and investment as well as easing supply-chain problems, have fueled strong US growth despite higher interest rates.

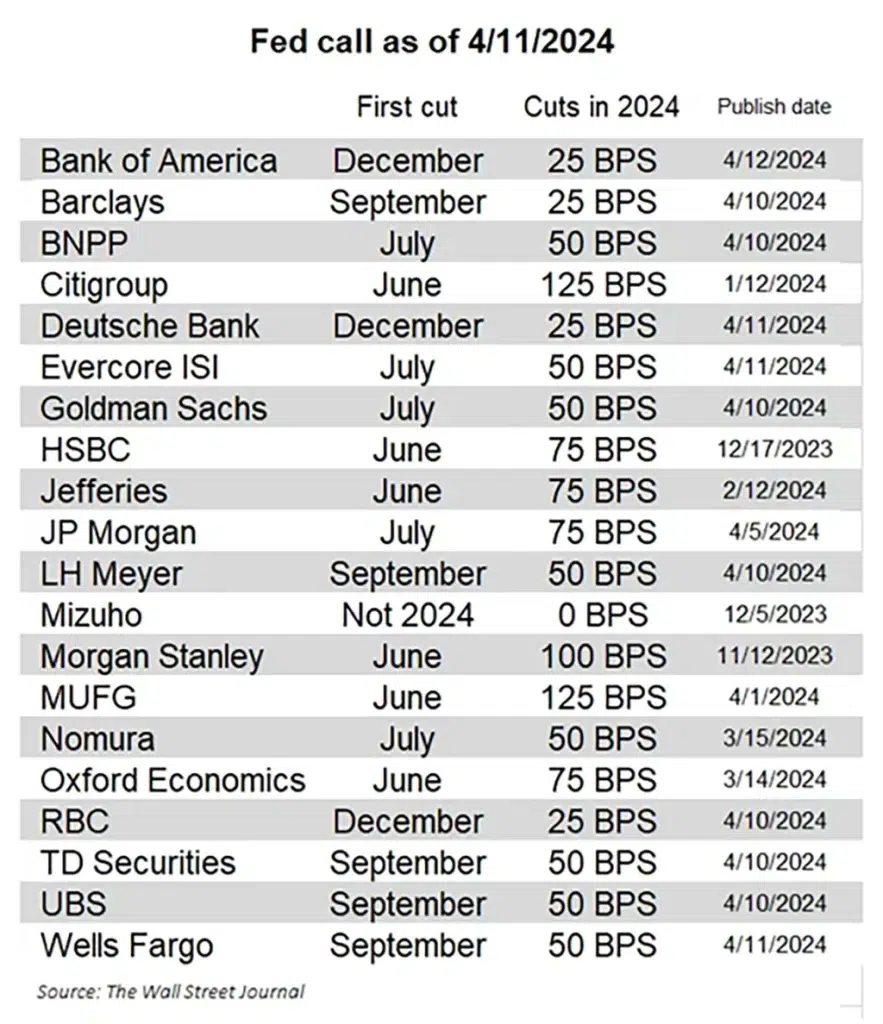

Most of the investment banks have recently changed their tune. We provide below a comparison of what the big banks are saying about interest rate cuts in 2024:

Market Uncertainty Will Continue

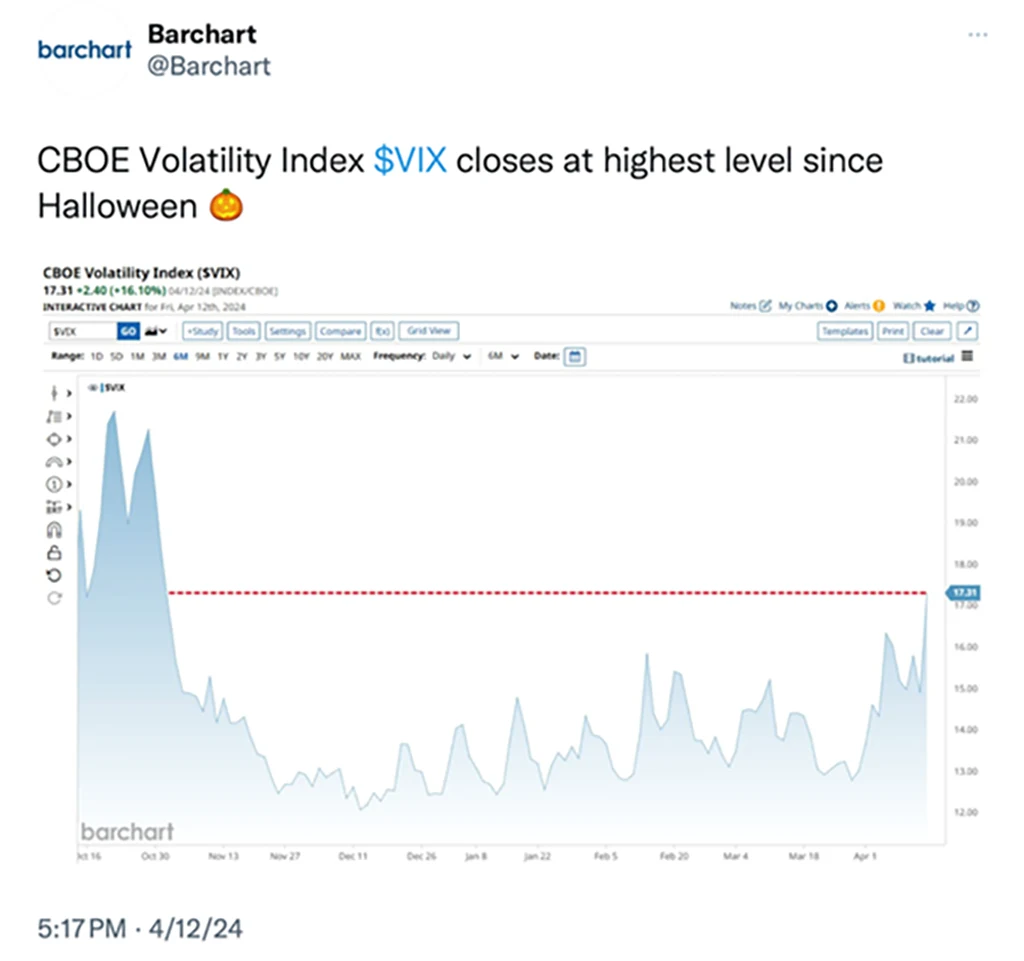

There has been a sharp pickup in the volatility readings indicating that fear is slowly creeping back into the markets. Given that Wednesday and Friday were two very volatile down days, we would expect this.

This is also being promulgated by the heightened geopolitical risk in the Middle East as well as Russia’s war rhetoric regarding NATO countries is not helping. We can see that both inflation and geopolitical risks are taking hold in the metals markets as Gold and Silver and even Copper are making new daily highs. (for Gold it is new all-time highs, but if you factor in the declining value of the US $ along with inflation, we are not yet really at all-time highs). See volatility (VIX) chart below:

{kind=link}