Weekly Market Outlook

By Donn Goodman

May 08, 2023

Welcome back readers, good to have you here.

It was a week filled with anxiety as the Federal Reserve was meeting and investors were awaiting their interest rate guidance.

Wednesday, Jerome Powell and Company announced that they were maintaining a “neutral” posture which for inflation hawks that meant no imminent hike in interest rates they had hoped would be the “next” action taken.

For optimists feeling that the Fed policy has been too restrictive, it provided hope that interest rate cuts would come in the near future.

Friday morning, the April jobs report was announced. The numbers (165,000 jobs created versus the 264,000 that were expected) demonstrated a real cooling in the employment markets with the unemployment rate jumping to 3.9%. This cooling off, coupled with the recently announced softer GDP growth (1.6% annual rate), was exactly what bullish investors wanted to hear.

Friday the stock market exploded higher making the bears retrench and cover their shorts and the bulls put more money to work. Technology was one of the big winners on Friday helped along by Apple announcing an enormous buyback of their shares during their disappointing earnings call on Thursday evening (phone sales fell by 10% during the last quarter).

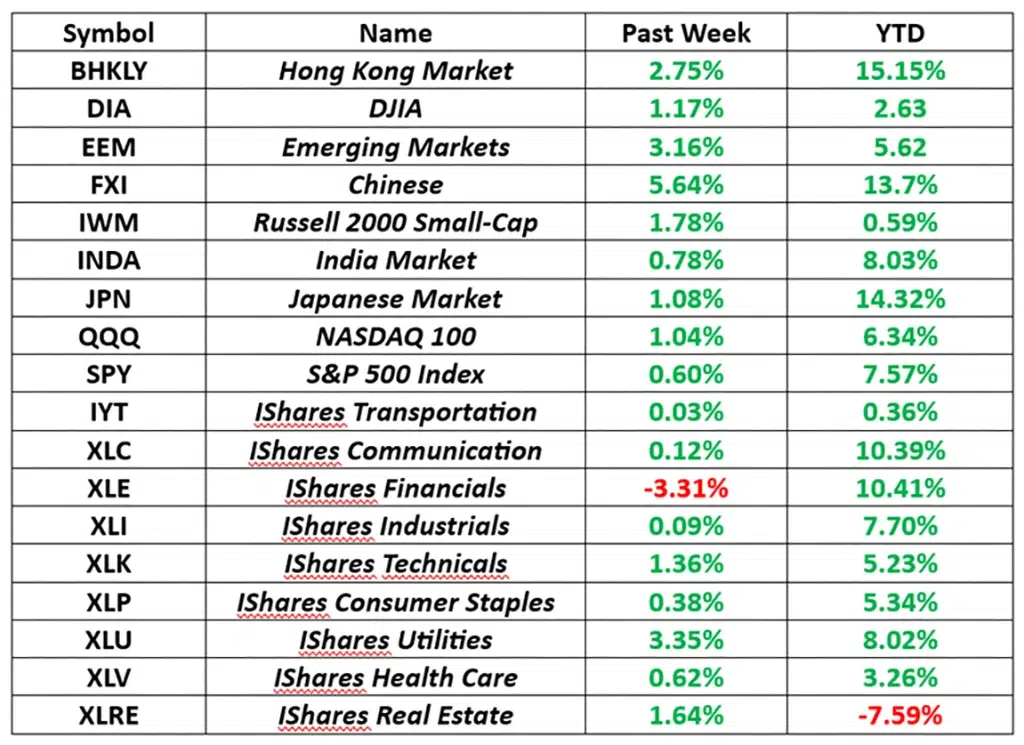

For the week, here is the scoreboard of different indices and specific sector ETFs:

I wanted to share the above with you because I thought that you might be shocked to see who the big winners were last week and the period since the start of 2024. Asian stocks, specifically China, Japan and Hong Kong stocks have had a long overdue rally that has surprised many investors.

Those market have also been helping to lift Emerging Market performance (China and Hong Kong are part of the emerging market narrative along with India). The big winner among US sector specific markets this past week was Utilities. I offer you a few charts indicating the strength of the Asian markets:

Don't Get The Weekly Newsletter? Join Here:

If you are a follower to Mish’s Daily, you know that she began to “talk up” Chinese stocks many months ago and gave her readers a Chinese stock to consider investing in. While she was early (she often is), those subscribers who read her Daily may be up as much as 20-30% on that stock alone. (Given that her Daily is free what is stopping you from subscribing if you are not already a follower? Go here to subscribe)

Also, when will you learn that you need only read this Market Outlook and Mish’s Daily to get good actionable ideas that can produce good investment winners!

Given the rising interest rate environment this year, it is surprising to investors that Utilities are one of the leading sectors, especially given the sector’s sensitivity to interest rates. Part of this is due to the expectations that interest rates will eventually come down along with the fact that we are experiencing warmer climates and higher energy consumption at the current moment. Utility companies have become much more efficient and are seeing higher revenues and a better earnings growth trajectory. This is certainly helped along by new sources of green energy, solar and wind power and innovative ways to deliver energy to high consumption businesses.

In MarketGauge individual strategies, we own a few of the Utility companies as these are in a growth phase and are also reaping the rewards of contributing to the blockchain marketplace as miners are consuming more energy than ever before.

If you would like additional information on these particular strategies that are benefiting from owning Utility stocks, mining companies, or if you would like information on our Bitcoin strategy (up over 50% year-to-date from using ETFs and Company stocks and not directly investing in bitcoin), reach out to Rob Quinn, our Chief Strategy Officer at Rob@MarketGauge.com.

If you also look closely at the table provided above you may be surprised to learn that technology stocks have not been the leaders in the market thus far in 2024, as they did in 2023. The surprise is that financial stocks (not this past week), energy and industrials have been more of the drivers.

With interest rates staying higher for longer (something both Mish and I have repeated for the past 6 months), the Real Estate sector is continuing to lose ground as lofty valuations from a low interest rate environment are being repriced.

Speaking of interest rates.

The good news on the interest rate front is that with Friday’s cooling job report, investors plowed into fixed income securities and rates came down from a high of 4.7% on the 10-year Treasury (and over 5% on the 2-year Treasury) to around 4.5% at the end of the week. That was part of the contributor to the big rally in stocks on Friday.

However, inflation hawks still believe that the Fed should raise rates one more time and that eventually, interest rates on the 10-year are headed over 5%. We are not so sure as the economy is showing signs of weakening, and that should put a lid on interest rates going forward. See chart of the rising trend of the 10-year Treasury rates below:

Given this rate rise over the past few months, April was very hard on fixed income investors. See graph below:

Use the link below to continue reading about:

- Earnings – 80% of the S&P 500 have reported and…

- Market statistics

- The BigView Bullets

- Keith’s weekly video market analysis

The market’s price action and news flow can be confusing and intimidating, but investing in this environment doesn’t have to be. If you would like personal guidance and hands-on management of your assets with the assistance of tactical, risk-managed, strategies, please contact me at donn@mgamllc.com or Keith at keith@mgamllc.com.

{kind=link}