August 16, 2023

Weekly Market Outlook

By Donn Goodman and Keith Schneider

We hope our Southern Boating readers have had an enjoyable week. Perhaps you are on vacation (like the rest of the world) or got to spend more time at the beach or your boat?

Before we tackle the many economic and stock market observations we will make, we want to reflect on the disastrous situation that occurred last week in Hawaii.

Our hearts go out to the people of Hawaii and especially Lahaina. We (and other friends) have spent time there. In our best recollection, like most of Hawaii, it was an older, beautiful community made up of gracious and kind Hawaiians, many of them natives who were committed to providing services to tourists who visit yearly. Most of these folks had small private businesses and were providing selfless service to visitors. Many of these people have nothing now. Over 100 souls have perished. Please keep their families and loved ones in your thoughts and prayers.

The economic data continues to show a slowdown.

The stock market was on edge earlier last week awaiting data on the CPI (Consumer Price Index) last Wednesday and the PPI on Friday. The PPI, (Producer Price Index) is the more closely watched indicator by the Federal Reserve.

The CPI rose 0.2% for the month of July and 3.2% on an annual basis. Excluding food and energy core CPI rose 0.2% month-over-month and 4.7% year-over-year in July. This was a slight downtick and softer than expected. (The market cheered).

The PPI in July rose 0.3% from the previous month and 0.8 from the previous year. This was a slight uptick and a bit “hotter” than expected. (Interest rates rose and the market was slightly down Friday and these negative sentiments continued into this week).

Weekly jobless claims rose by 21,000 from the previous week bringing the total for August 5th to 248,000, higher than expected. This also showed that the employment picture is beginning to slow.

Oil inventories rose by 5.9 million barrels last week, but crude oil prices rose $2.21, ending the week at $82.76 per barrel. Energy prices have been trending higher. This is concerning, as it inevitably will put pressure on the upcoming month’s inflation readings. Energy prices continue to hit consumers in their wallets. Analysts also believe this is directly tied to retail. Consumer discretionary and retail stocks are showing signs of weakness and a slowdown in spending. See oil chart below:

As we demonstrated last week, interest rates (specifically the 10 and 30-year) are trending higher. Much of the above data is tempering proof of any kind of slowdown that the Federal Reserve has been working towards. If anything, some of those numbers (PPI ticking up) are pushing interest rates higher (the 10-year rate is close to a new high). Are we seeing a top in interest rates or a breakout with higher rates to come? See chart below:

Inflation expectations.

Chairman Powell of the Federal Reserve always includes language in his speeches and post Federal Reserve meetings about CONSUMER INFLATION EXPECTATIONS as a leading indicator for actual inflation.

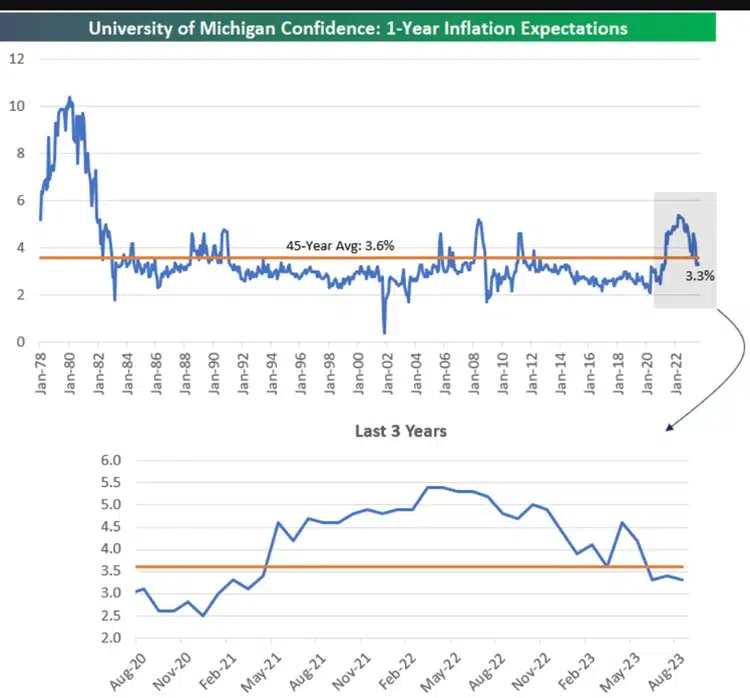

One of the main reads on inflation expectations comes from the University of Michigan’s Consumer Confidence survey. The most recent University of Michigan survey came out Friday morning. It showed that consumers’ one-year forward inflation expectations are now at 3.3% year-over-year. This was below the consensus economist’s estimate for a reading of 3.5%.

What is most significant about the 3.3% number is that it is below the 45-year average reading of 3.6%. This means that consumers have gotten more sanguine about inflation compared to last year when these same readings routinely came in above 5%. See charts below:

What this more importantly implies to us is that the average consumer believes that the economy is going to slow down over the next few years. This may be primarily because they are feeling the “pinch” themselves and believe something has to give. Most consumers do not think the rise in prices is sustainable. This also implies that many consumers might think a material slowdown or even recession is in the cards. This figure can cut both ways, positive and negative.

The Dog Days of August.

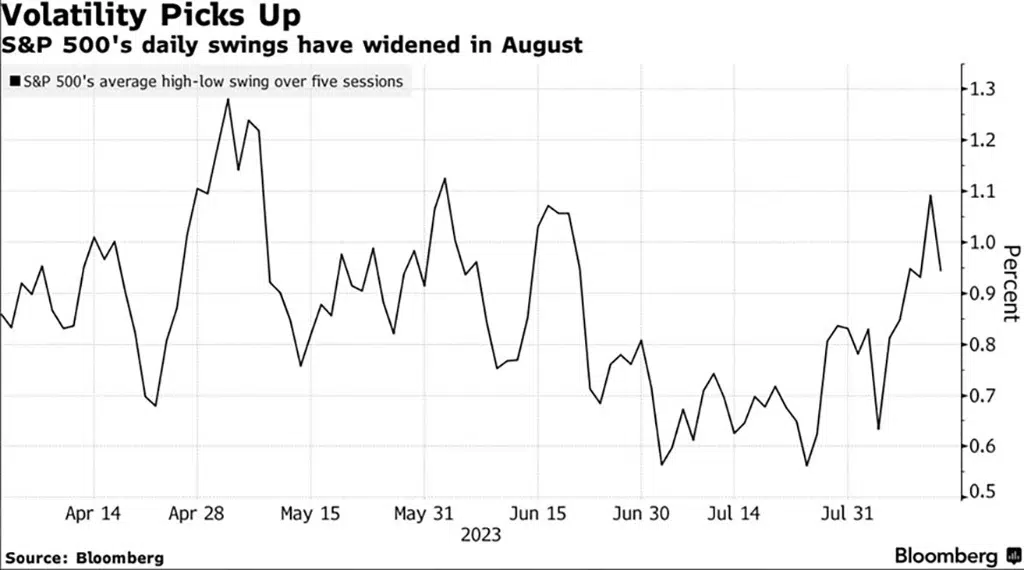

As we noted last week, we are seeing the signs of the summer trading malaise. This is probably why good news sends the market higher than expected and negative news sends the market further down, as it did so Tuesday. These moves are exaggerated by the lower trading volume. These lower volume days and weeks typically push volatility higher.

As noted in last week’s Market Outlook (if you missed last week’s commentary, here is the link), volatility usually picks up at this time in the summer. See chart of recent activity below:

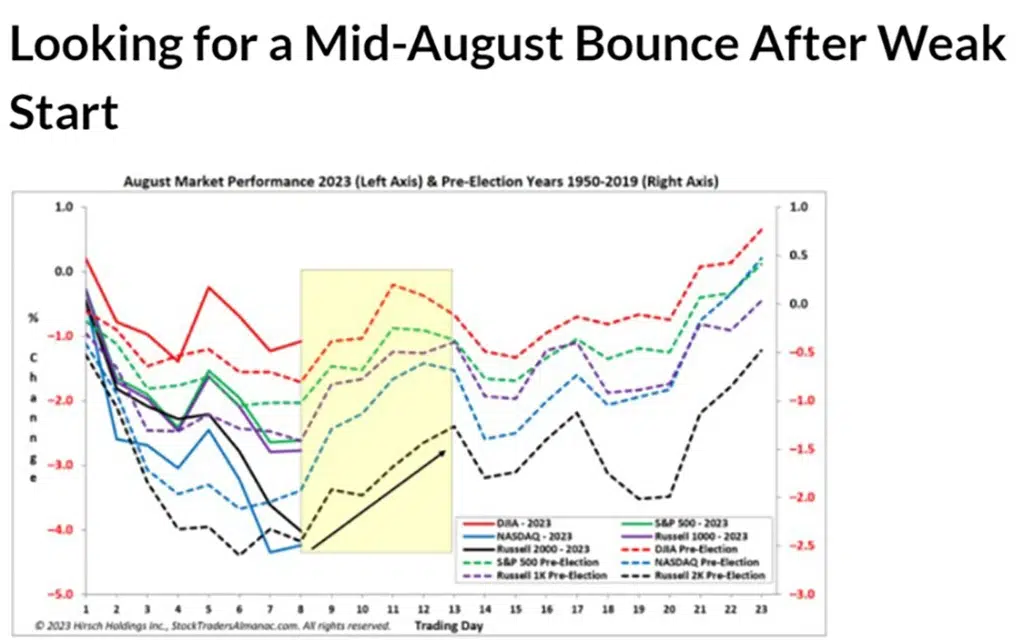

Last week we also showed a few charts indicating the seasonal weakness of August and September. While pre-election years (the 3rd year in a Presidential Election Cycle) are almost always positive for the S&P 500, the seasonal weakness in late summer and early fall, typically happens.

Last week ended with a whimper as the S&P 500 and the NASDAQ ended slightly lower and the Dow notched another positive week. See more on the NASDAQ below. This investment period, in pre-election years, is typical to find a CONSOLIDATED market digesting the gains made in the previous 7 months.

What's the Stock Market's Next Move?

Remember that we are in a pre-election year and while these years are almost always positive for the stock market (S&P 500), there is typically a seasonal soft period during August to October. Such is the case this year as well.

Some analysts believe the economy still shows robust strength and are not expecting anything other than a shallow pullback. As mentioned above and throughout this week’s column, it is not unusual to see sideways to down action in August and September.

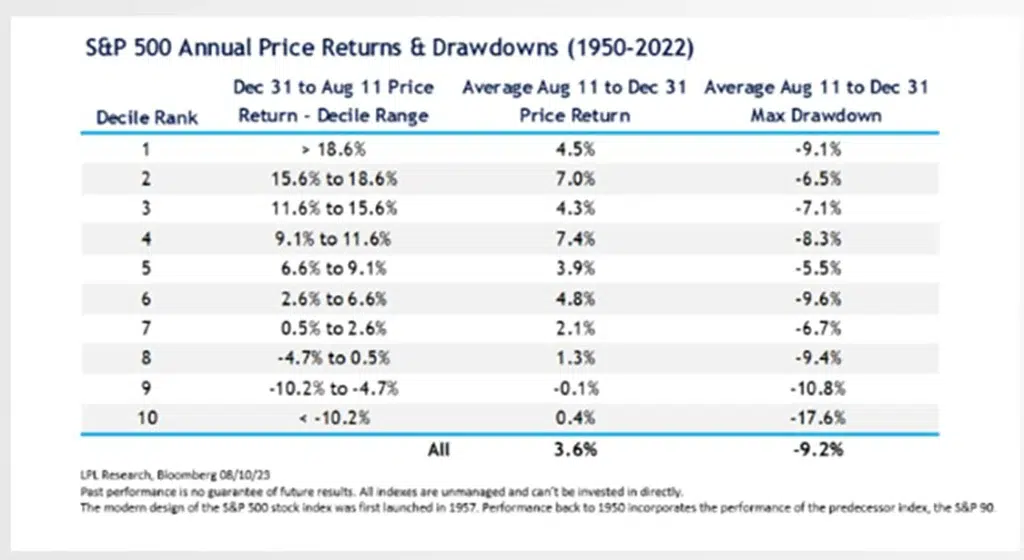

Looking at historical returns for the 3rd year of a Presidential election cycle, you can see that so far this August we have tracked closely to the historical average. See charts below:

Last week ended with a whimper as the S&P 500 and the NASDAQ ended slightly lower and the Dow notched another positive week. See more on the NASDAQ below. This investment period, in pre-election years, is typical to find a CONSOLIDATED market digesting the gains made in the previous 7 months. Actually, we are right on track. See chart below of the typical pre-election investment year:

August has its own historical cycle bias. If history is any indication, we should get a bounce sometime over the next 1-2 weeks. See chart below:

{kind=link}