Welcome back readers. Hope you weathered the market storm this past week as we started off September with a big down move.

Last week we wrote about the new highs (blue skis) but also the possible September swoon that often occurs this month. We highlighted the past four Septembers and their consecutive negative performance months. If you have not yet read last week’s Market Outlook or wish to reread it, you can get it here.

You may recall that we described what typically happens after Labor Day when portfolio managers return from their summer getaways and long extended holidays, buckle down and start rebalancing and rotating in/out of companies that look more promising.

Given the technology sell off which began in mid-July, it is apparent that there has been a rotation going on into more “value” oriented stocks which include financials, utility, and recently consumer staple stocks. These are typically considered defensive stocks. Given the non-farm payroll revisions in the past few months (almost 1,000,000 less jobs created) and the monthly job created misses, it is no surprise that portfolio managers are beginning to prepare for an economic slow down. More on this shortly.

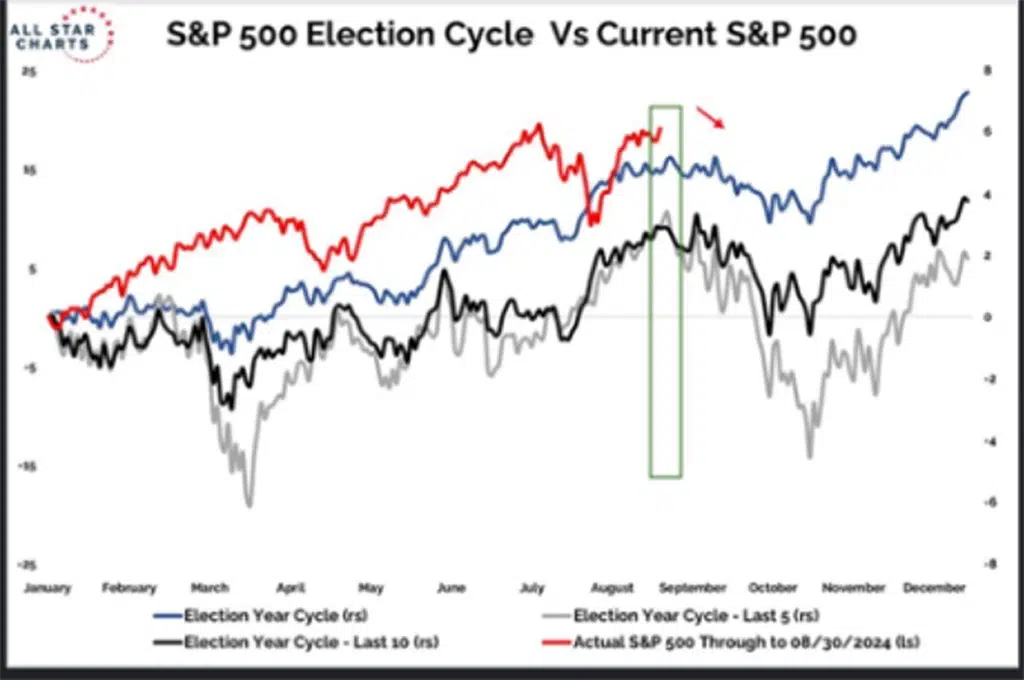

It’s a tough time of year for stocks

As we’ve mentioned, it’s a tough time of year for stocks, and election years don’t help as you can see by the chart below.

This widely-known seasonal trend may increase the market’s volatility as digests the current events discussed below.

A big down week.

This was a shortened week due to the Labor Day Holiday. However, stocks began a brutal sell-off from the opening bell on Monday and followed through to market close on Friday with 4 negative days.

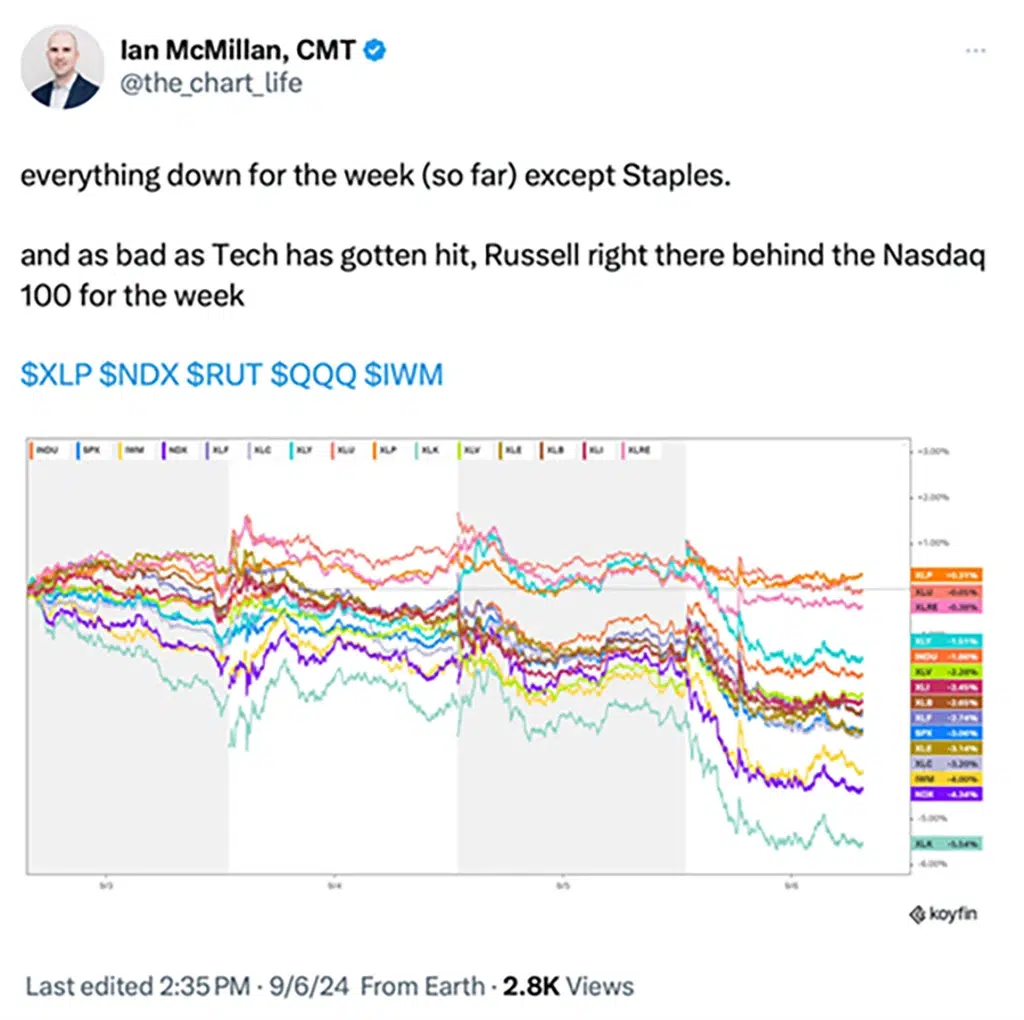

The S&P 500 (SPY) had its worst week since March 2023 (the bank crisis) and was down 4.1%. The NASDAQ (QQQ) followed suit and dropped 5.8%. This was the worst week for the NASDAQ since the bear market lows of October 2022. The Russell 2000 (IWM) small cap index was down 5.5% as investors abandoned the smaller companies. This is an area of the market that would normally benefit from a potential reduction in interest rates (more on this shortly) as investors see a more serious slowdown ahead.

While the S&P 500 is now down -4.5% off its record high, the Nasdaq is down twice as much, -10.9%. This weakness is appearing right on time as we have previously pointed out, September has notoriously been the worst month for stocks.

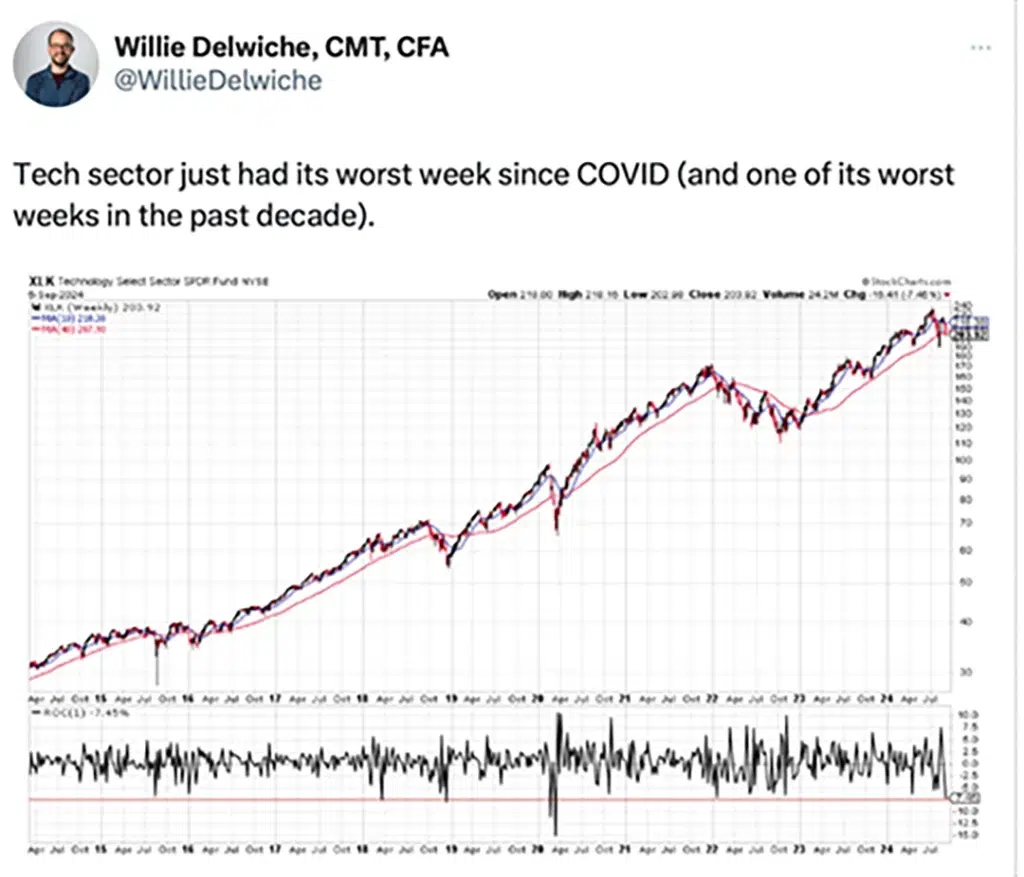

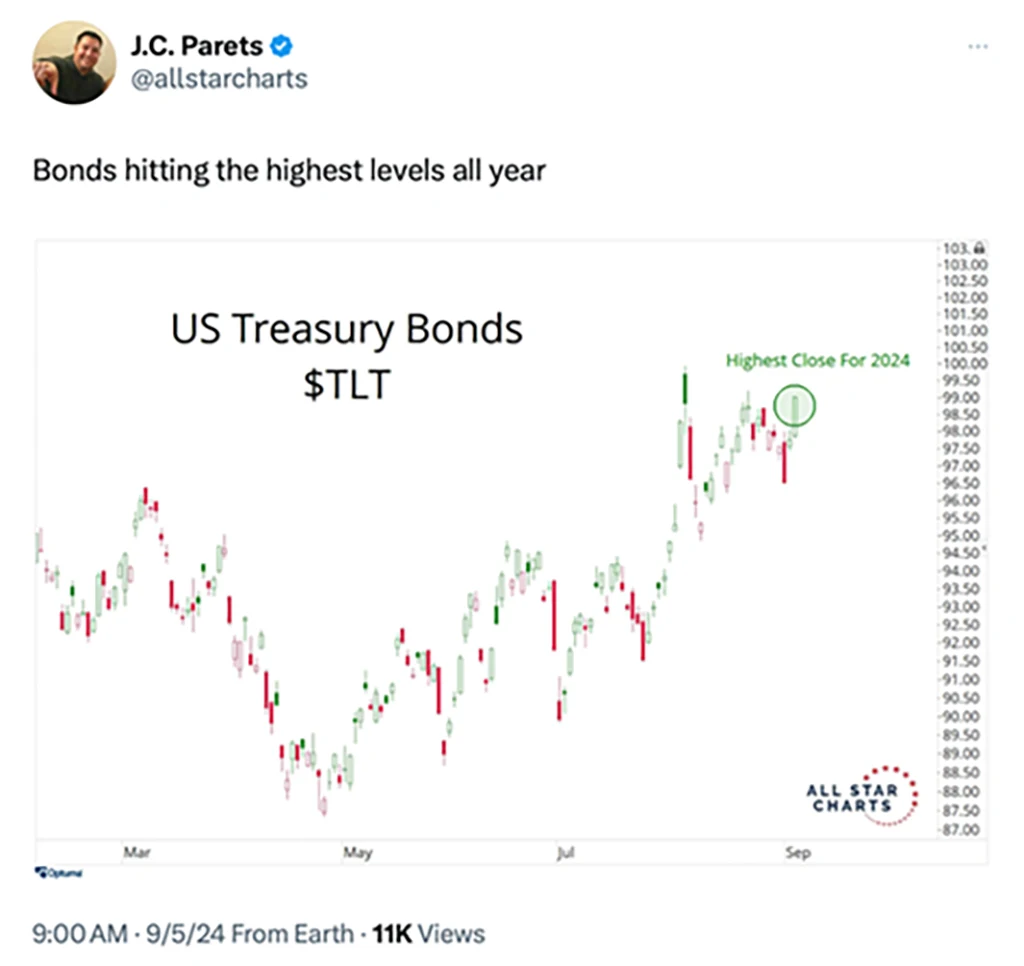

The largest sector of the S&P 500, technology (XLK), had its worst week since the COVID pandemic, declining -7.5%. The Bond market rallied as did Consumer Staples, both defensive sectors, as we saw a clear flight to safety. See charts below that illustrate the negative week for investors:

Regarding technology stocks, it was the semiconductor stocks that led the sell off back in July and most certainly this past (shortened) week. The semiconductor sector ETF (SMH) was down 11.5% for the week. Additionallly, another major chip company, Broadcom (AVGO) announced disappointing earnings and investors could not sell the stock quickly enough.

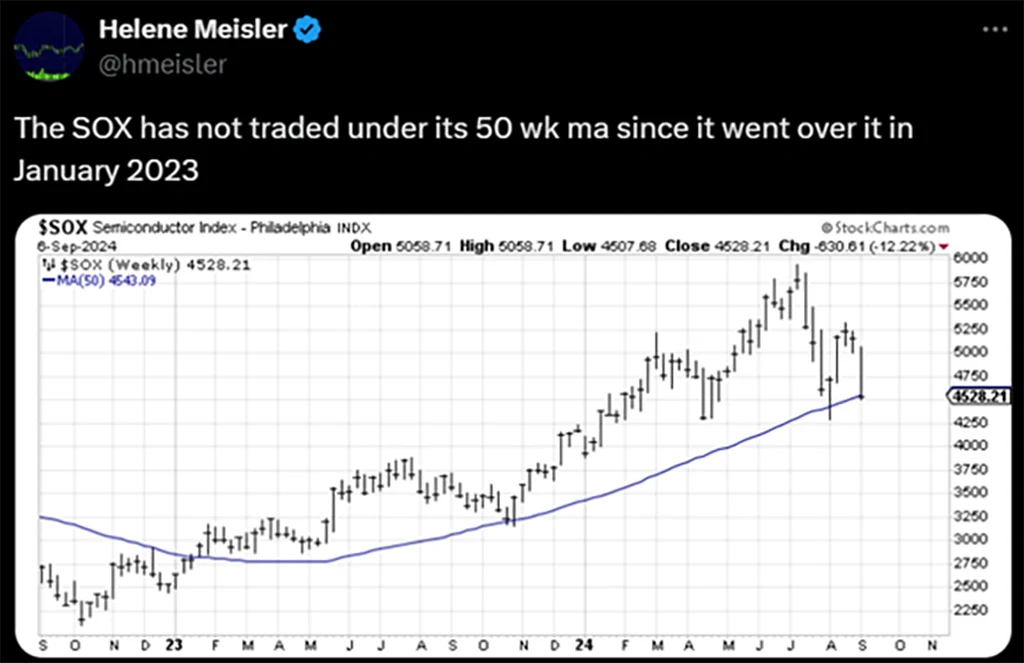

The semiconductor index (SOX) sits precariously at its 50-day moving average. Is a bigger breakdown coming? See chart below:

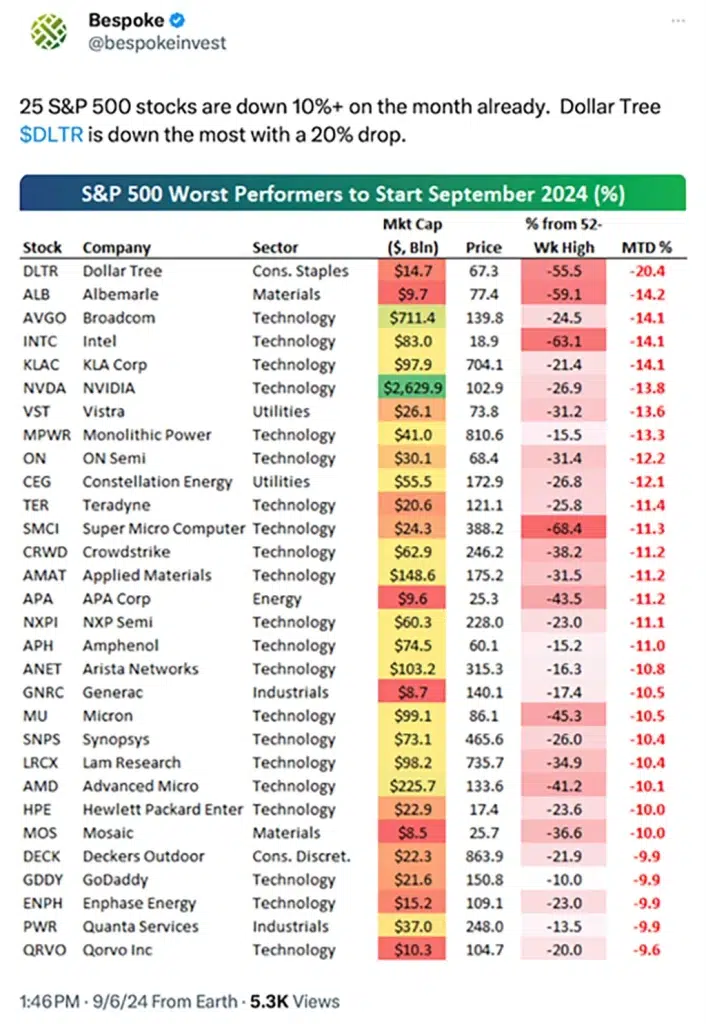

To see exactly how brutal the MTD (month-to-date) has been so far, we provide the following table of the worst 25 stocks for September. You will notice that technology makes up the biggest share of companies that are getting clobbered thus far. There are 9 semiconductor companies on this list. See chart below:

Investors would have to ask, “Is the AI trade done?”. We are not sure, but ChatGPT did report that far less people are coming to their website and that traffic and inquiries have slowed. Many of these tech AI companies are also expressing that they are “laying off” employees and beginning to slow cap ex given the potential economic slowdown we are facing. (more on this shortly).

What concerns this writer is the number 1 stock up above. That is Dollar Tree. Along the same lines are other retail stocks, Dollar General, Dicks Sporting Goods, Five Below, and possibly even Amazon (AMZN), which has begun to look vulnerable. These retail stocks are the giants of middle America and have all announced disappointing earnings and have all seen implosions of their stock prices.

Additionally, credit card delinquencies accelerated to over 9% this past month, further cementing the idea that consumers are tapped out and have exhausted any leftover stimulus from the pandemic. See retailer stock laggard charts below:

{kind=link}