Welcome readers. We hope you had a profitable and productive last week of January and first few days of February.

The End of the Month Period.

The end of the month is a uniquely favorable period for investing. A number of factors contribute to this, including 401k contributions getting invested, companies typically buying back their stock towards the latter part of the month, pension funds rebalancing their asset allocations, and some individuals having auto investment plans.

Combine end of month favorability and the continuation of a bull market that blasted off at the beginning of November when the Federal Reserve broadcasted upcoming rate cuts, and it is no surprise that the market remains in party mode.

It is also earnings season (more on this shortly). Couple the favorable positive seasonality with blowout earnings from several of the largest tech companies, and you have the recipe for the party to extend further. But will it continue? We will explore a few charts and commentary about the upcoming (election) year and what the current earnings season and market pricing may hold going forward.

Therefore, it is no surprise that the end of January and the beginning of February have, so far, been positive.

Did you know that MarketGauge utilizes a strategy that invests only 32% of the time in the markets and takes advantage of calendar and seasonally positive periods? This strategy has a back-tested and partially real-time track record with over 8.5% a year return for 6 years with minimal drawdowns.

We also recently received a positive signal from one of our other investment strategies, Profit Navigator, and entered the market with a partial position. The unlevered strategy has back-tested at over 17% a year with drawdowns of less than 40% of the S&P 500. The levered strategy interestingly enough has back-tested at over 32% per year with drawdowns slightly less than just investing in the S&P 500.

If you would like more information on these strategies or how we can put them to work for you, please contact Rob@marketgauge.com or set up a free strategy call at www.marketgauge.com/call.

Two important economic inputs this past week.

On Wednesday, the Federal Reserve Chairman, Jerome Powell, told the markets that there would be no change to interest rates, which fell in line with economists’ and market watchers’ predictions. He also stated that it was unlikely that the Fed would lower rates in March. That took some investors by surprise and resulted in an immediate sell-off which reversed course by day’s end and had little negative influence the remainder of the week.

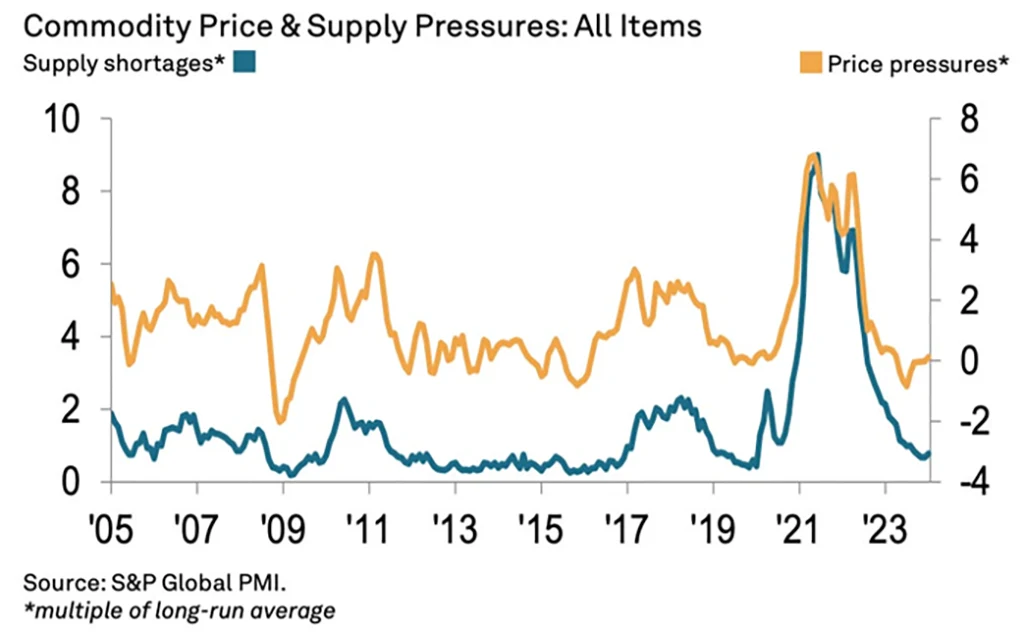

The Federal Reserve continues to aim for the proverbial 2% inflation rate. As we showed in last week’s Market Outlook (if you have not had a chance to review it, click here), inflation has come down at a rapid rate. One of the reasons for inflation falling so fast is that the supply chain has been “fixed” and commodity prices have plunged. A good illustration of this is the following chart:

The Fed’s Pause

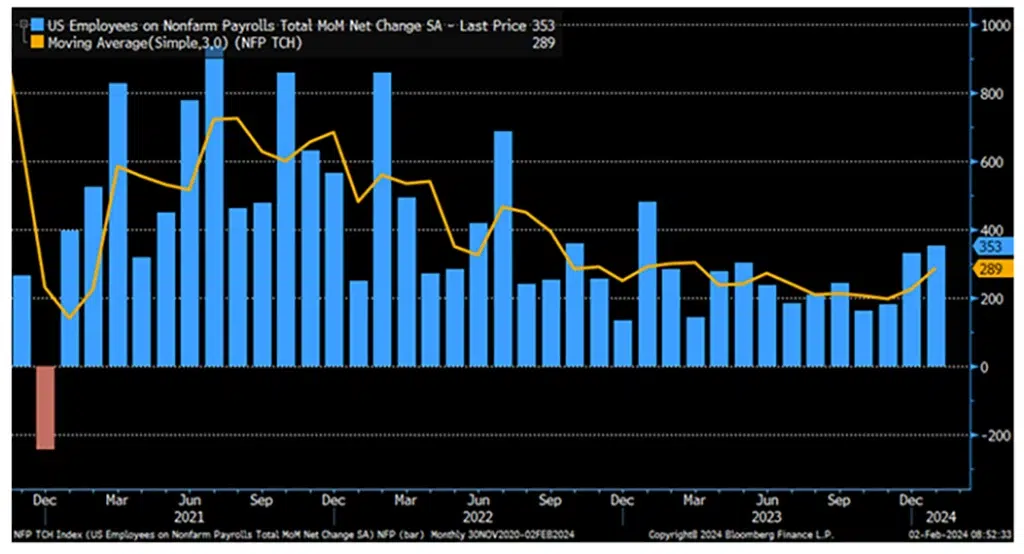

As we stated above, the Fed’s pause was not a surprise. December payrolls added 216,000, and the CPI, which measures inflation, came in at an annualized rate of 3.4%, well above the 2% target rate. Then, on Friday, the jobs report was SHOCKING with an announcement that came in at 8:30 a.m. (before the market opened) with 353,000 new jobs added in January. This was over 2x the expectations given that ADP announced their household report of only 107,000 new jobs earlier in the week. The unemployment rate declined to 3.7% from an expected rate of 3.8%. Interest rates, which had been slowly coming down, reversed course and ended the day over 4% for the 10-year Treasury.

Who to believe? We are not sure that the Bureau of Labor Statistics report of 353,000 could be accurate given that the ADP report was actually obtaining accurate information from households. Many believe the ADP report more accurately reflects the job market. Also, the 353k number could include people who are working multiple jobs and being counted several times.

The positive number that was released on Friday (and may have been the silver lining) was the Employment Cost Index, which only increased to 0.9% and shows that labor costs are slowing dramatically. This number suggests that employers are feeling less pressure to raise pay to attract and retain workers as wage growth slowed in the 4th quarter of 2023. These numbers show a possible reacceleration of the economy.

Conclusion on interest rates: Last year, in this column, we commented frequently that we believed interest rates would stay higher for longer. Now we continue to believe that the economy is not showing nearly enough signs of weakness to warrant the Fed to lower interest rates until later in the year.

We also remain concerned that inflation may reaccelerate, especially given the turbulence in the Middle East and the effect it could have on the price of oil. The market has adjusted its expectations to only a 20% chance that we could see a March rate cut. While June remains at a 60% chance, we wouldn’t be surprised, given the strength in the economy, if that rate cut is also pushed off a few months.

However, another point of view worth considering is that the Fed may wish to help the current administration get reelected (or feel the pressure to do so). There may be a high probability that they are going to cut rates mid-year to create easier financial conditions going into the election.

The Market Party lives on.

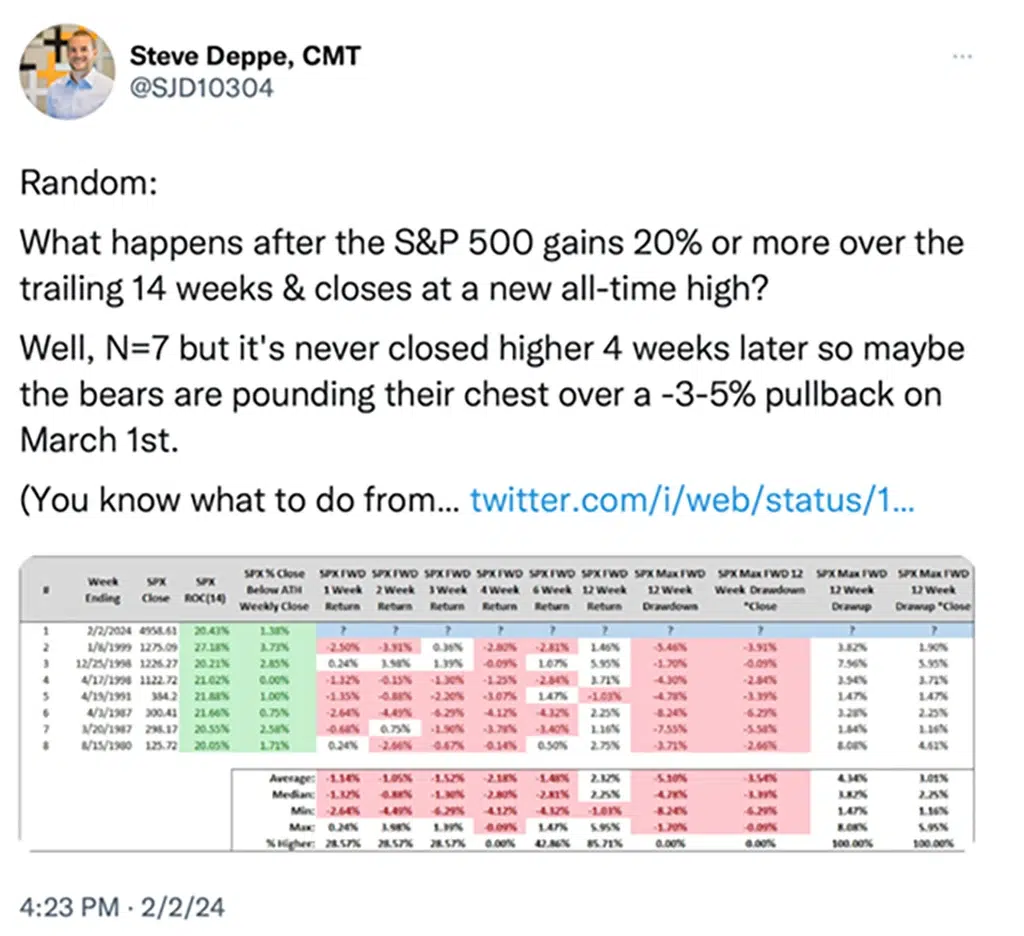

- The S&P 500 closed at an all-time high for the third consecutive week and is now less than 1% away from hitting 5,000 for the first time.

- Since the October low, the S&P 500 has closed higher in 13 of the past 14 weeks, gaining 20.4%. See chart below:

Is it a good time to put capital to work in the stock market?

Friends and clients always ask this question. It is a good one. Up above, we showed that after hitting a new all-time high after 14 weeks (and a 20% gain) the markets were lower 4 weeks later. This may or may not happen this time.

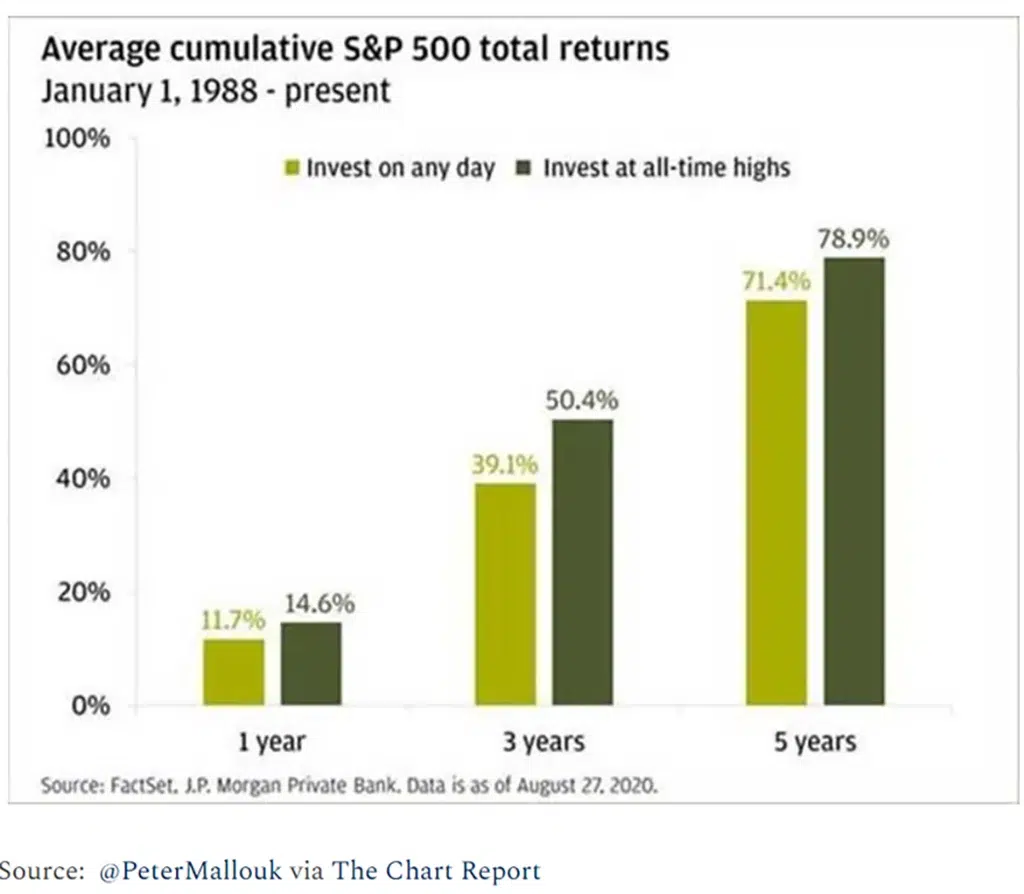

Statistics point out that investing in the market after it hits a new all-time high tends to reap further gains. Additionally, investing after a positive January has good follow-thru potential.

At MarketGauge, we offer subscribers and asset management clients various investment strategies and blends that incorporate different market-beating investment edges. Even if it were not the best time to get invested, our strategies are intended to help minimize risk and rotate into more favorable areas of the market.

{kind=link}