Welcome back readers. Thank you for a few minutes of your time to uncover some important takeaways on the markets and the economy. While we cannot accurately prognosticate what the markets may do going forward, we have been on the “right side” of our observations and suggestions throughout 2024 in this weekly outlook.

The last two weeks, even with a negative market, we provided plenty of reasons why you might want to stay on the long side of the market. These included impending economic softness (soft landing), unemployment increases, good to great earnings, election year influence, seasonal (July and August) positive historical periods and optimism and momentum that has been driving the market. (If you have not read or you wish to review the past two weeks of Market Outlooks, you may go to the link provided here)

We want to continue with this theme and provide notice that we are getting closer to September, an important National Election and what many believe is a tenuous period for stocks. Let’s jump right in.

Good economic numbers and a “soft landing narrative” drove the markets higher this past week.

You certainly will recall that as we took the turn from July to August and with the release of important numbers like job growth, unemployment, and the ISM, stocks broke down (quickly), and the discussion on Wall Street was about the potential for a recession. In fact, the first week of August many economists were pontificating that the Fed needed to have an emergency meeting and lower rates immediately. So much for that narrative.

We were met with a quick pullback/correction (more on this shortly) and the markets turned on a dime two weeks ago and began to head up. Our view these past few weeks was that much of this was driven by a liquidity shock crisis driven by large institutional managers and hedge funds who had to sell securities to meet margin calls from the Yen carry trade. Surprisingly, many of them got adversely caught in this scenario after the Bank of Japan raised rates suddenly to offset their own revised growth and inflation.

Good economic numbers.

Before we address just how good the stock markets did this past week (the best week of the year), we want to point out that much of the prior period’s weakness was driven by investor concerns that the Federal Reserve wouldn’t reduce borrowing costs fast enough to keep the US economy out of a recession.

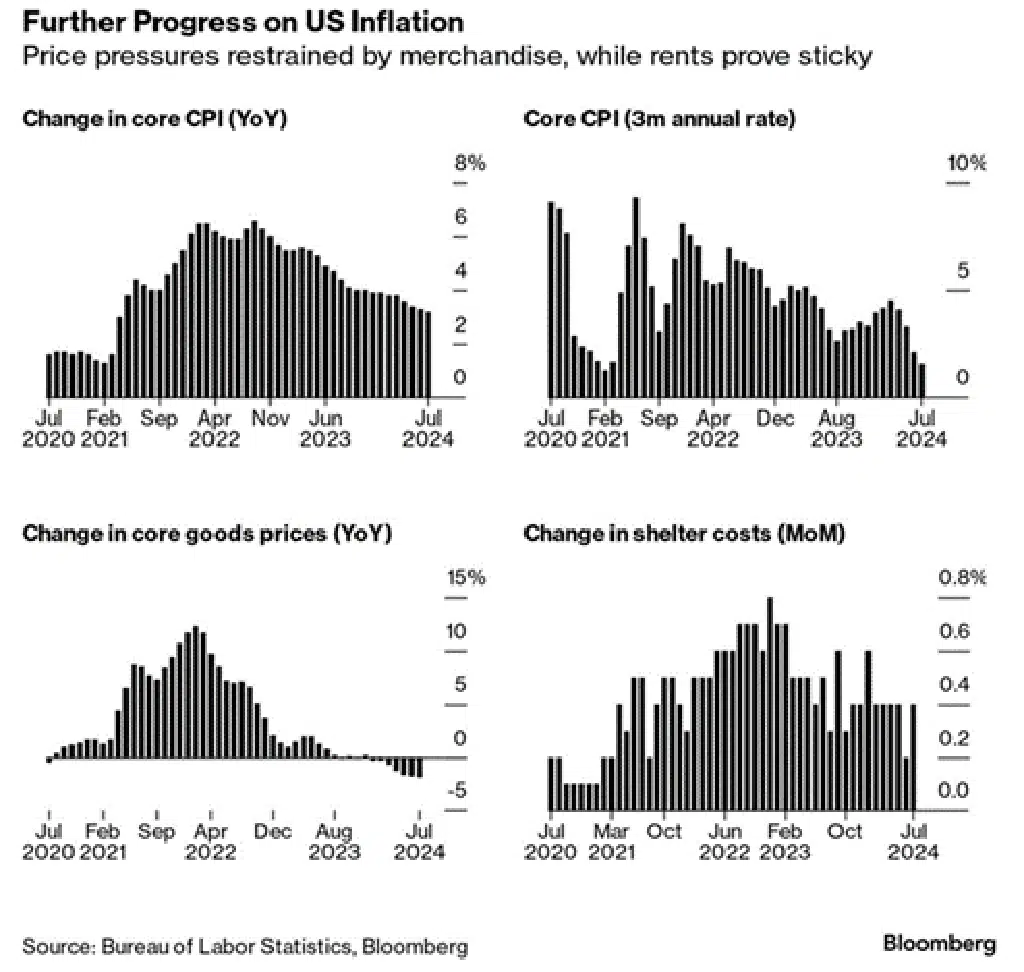

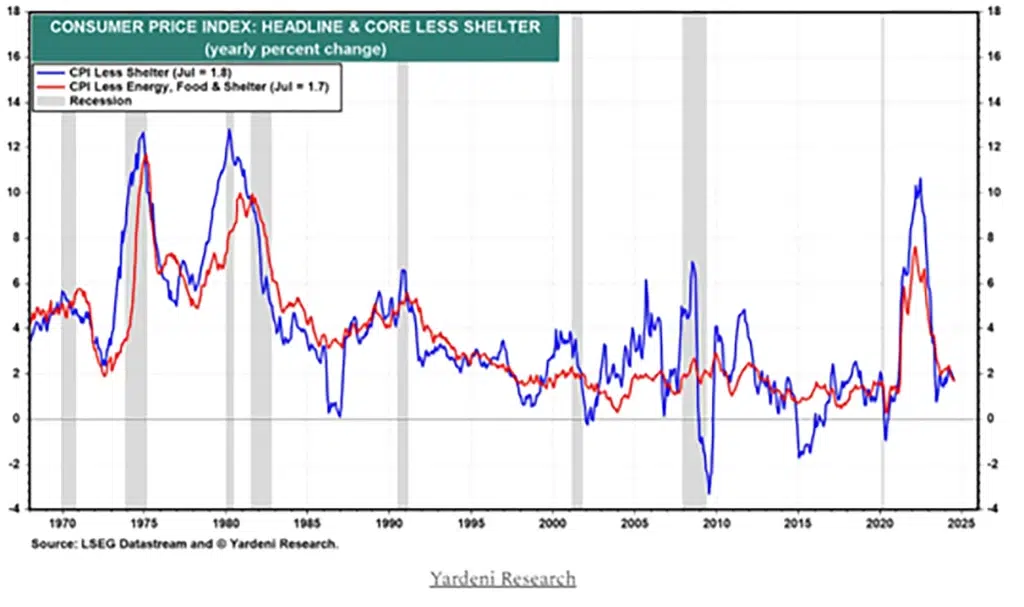

But new data this week showed ebbing inflation and a resilient and thriving consumer. These are the hallmarks of the Fed’s goal of a soft landing. The CPI came out and showed that the economy continues to cool down which should motivate Jerome Powell and company to commence with a rate reduction schedule in September. See CPI illustration below which identifies the specific areas of the CPI that continue to decline/cool:

Consumer sentiment rebounds.

This past week we also received an update on the University of Michigan consumer sentiment index. The index jumped in August and surprised to the upside. It was the first increase in five months. Part of the surprise was the consumer expectation for 12-month inflation declining to the lowest level since December 2020.

On Friday we received the numbers showing an unexpected rise in retail spending. The Commerce Department’s release of sales of US retailers in July rose by a solid 1% from the prior month. This is the backbone of America’s economy, and this proved that we are unlikely to enter a recession anytime soon.

This was welcome news and helped the S&P 500 surge to a new monthly high and into the green for August.

Two important sectors that are vital to the US economy.

I always like to refer to Mish’s Economic Modern Family and the influence of each member on the health of the economy and the markets. Two important (crucial) characters that often point to the health of the markets are Granny Retail and Sister Semiconductor. Below are two price charts for these sectors.

Notice the snap back this past week in the retail sector. While it has not made a new high for some time (actually moving sideways in a rectangle box), it continues to show the consumer’s resilience by staying above the 50- and 200-day moving averages.

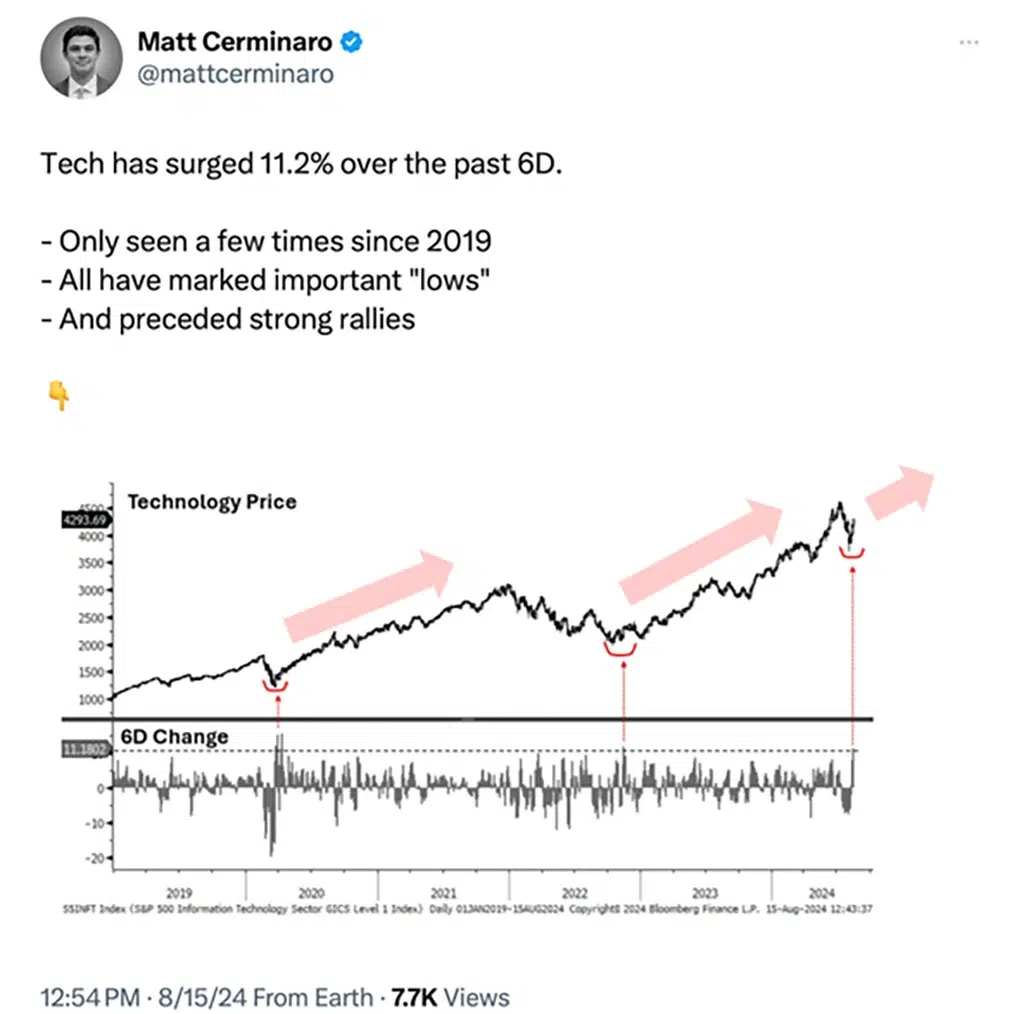

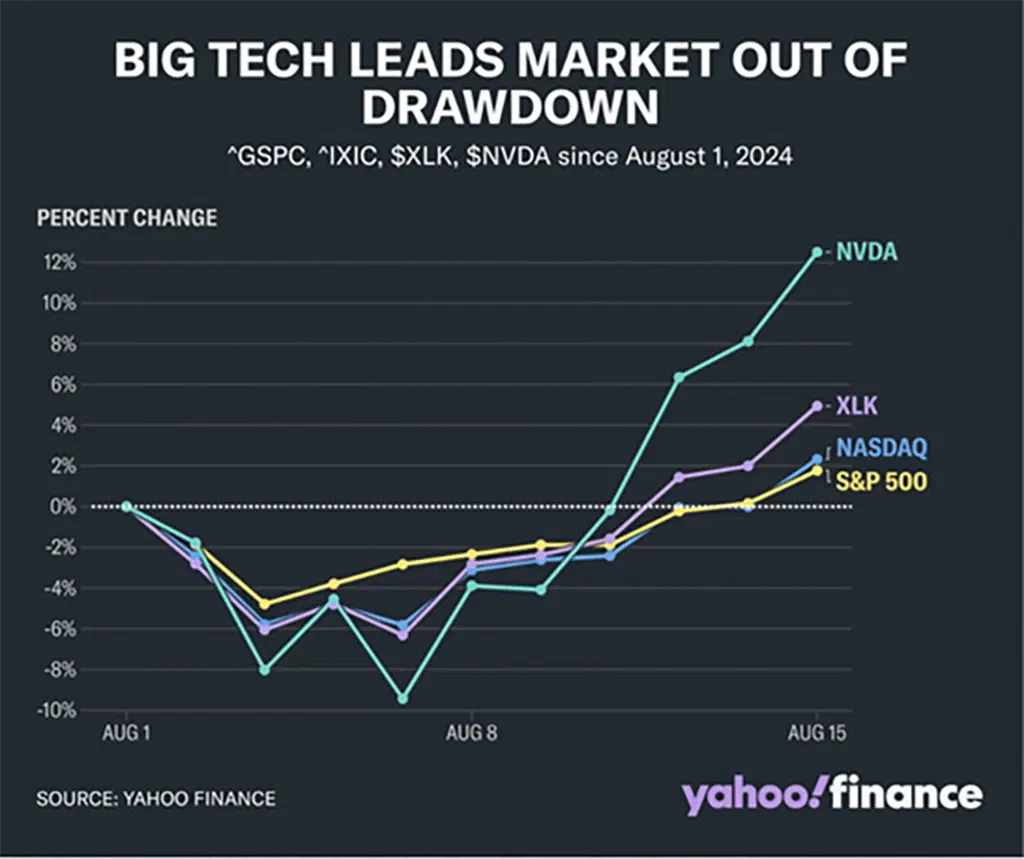

A similar positive tale now for the semiconductor stocks (Sister Semiconductor) below, although the price action remains below the 50-day moving average. More on the tech stock rebound in a minute.

{kind=link}