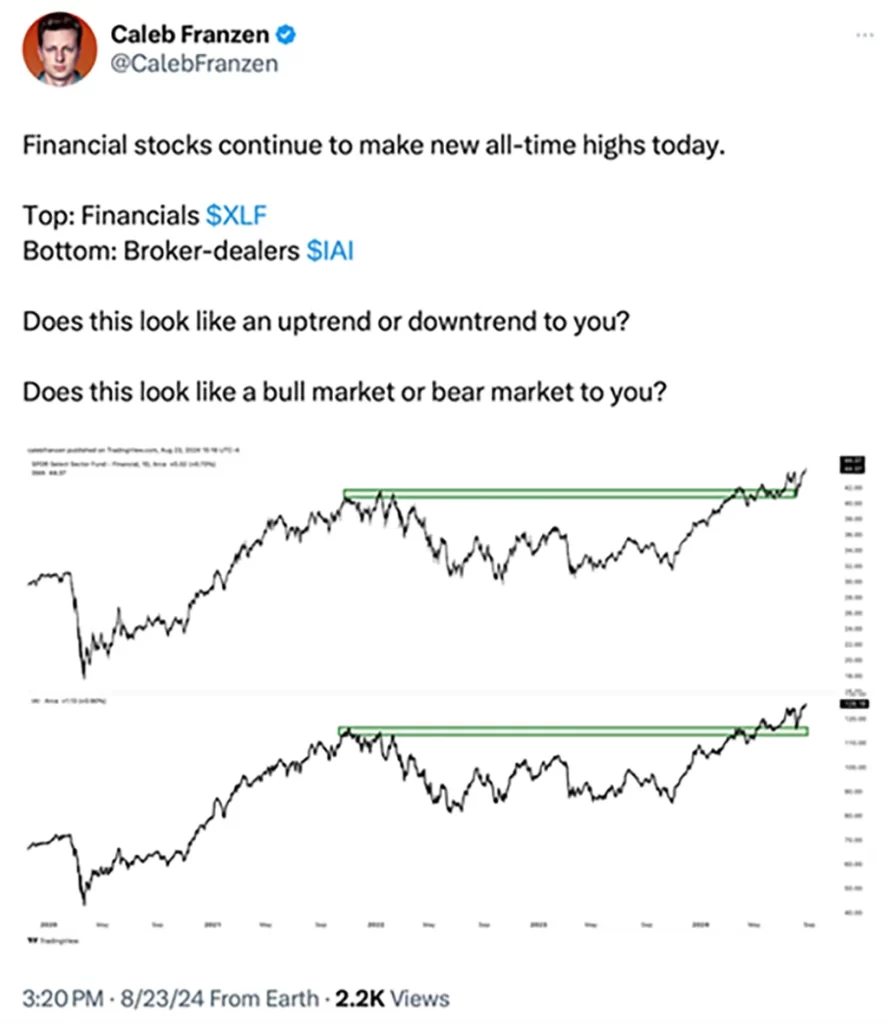

Welcome back readers. We are glad you have joined us. We hope that you are enjoying these longer summer days accompanied by the recent positive weeks in the stock market.

“The time has come for policy to adjust. The direction of travel is clear. My confidence has grown that inflation is on a sustainable path back to 2%.”

These were the words that Jerome Powell used on Friday at the annual conference in Jackson Hole, Wyoming. (I don’t think any of us could realize just how important the Jackson Hole conference has become). The stock markets positively reacted Friday with a sigh of relief. There had been somewhat of a negative anticipatory feeling on Thursday as many pundits grew concerned the Federal Reserve might not become quite as “dovish” as those words above indicate.

You will recall that two ½ years ago, the Federal Reserve embarked on an aggressive tightening policy to bring down inflation. The Federal Reserve hiked borrowing costs to crush pandemic-spurred inflation. Additionally, in 2021-2022, an acceleration in government spending and a curtailing of energy development exacerbated the situation, and inflation took a long time to start on a downward path.

Higher interest rates over the past 24 months have crippled many sectors of the economy, including home buying and borrowing for small companies that rely on regional banks for business expansion. The calls for the Fed to lower rates began in earnest late last year and have been repeated throughout 2024. But the Fed stuck to their guns and proclaimed that their overnight rates would stay “higher for longer.”

I guess us old timers in the market remember the 1970’s all too well and how stubborn inflation can be to bring down. All of us as consumers (especially of rents and food) understand this recent cycle of inflation has been punishing. Many families in the US have a hard time being able to afford to put food on the table.

Mish and I have consistently said that the Fed should keep rates higher and avoid being premature in lowering them, thus spurring on potentially sticky and lingering inflation. In the face of them lowering rates to avoid a hard landing, the possibility of elevated pockets of inflation remains. I have covered some of these points and more the past two weeks in this column. If you have not yet read these Outlooks or want to go back and review, you may do so here.

The Federal Reserve’s Job.

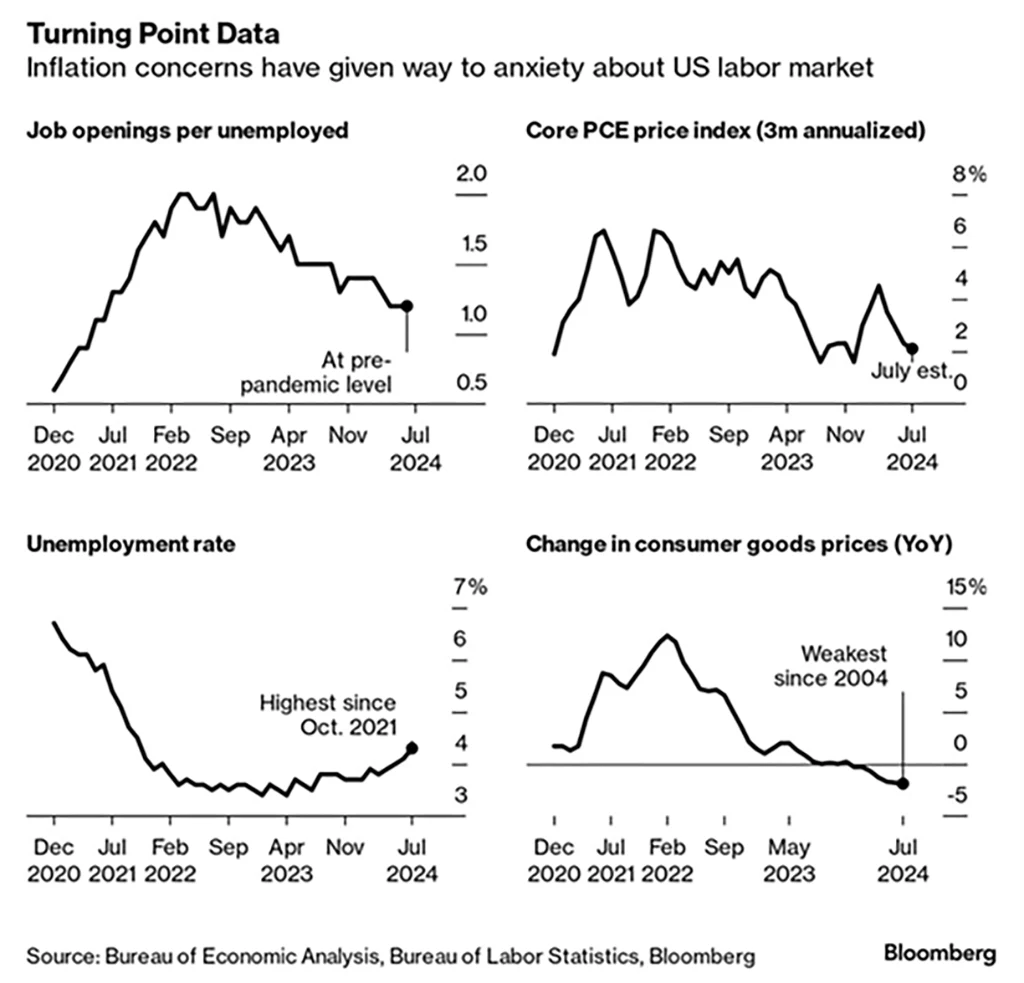

Just to rehash the Fed’s job here, they have a dual mandate to maintain price stability and to achieve maximum employment. Their view of whether interest rates should be increased or decreased is always dependent on the data. That said, there are now clear signs that the labor market is weakening, as it has recently risen to a 3-year high of 4.3% unemployment.

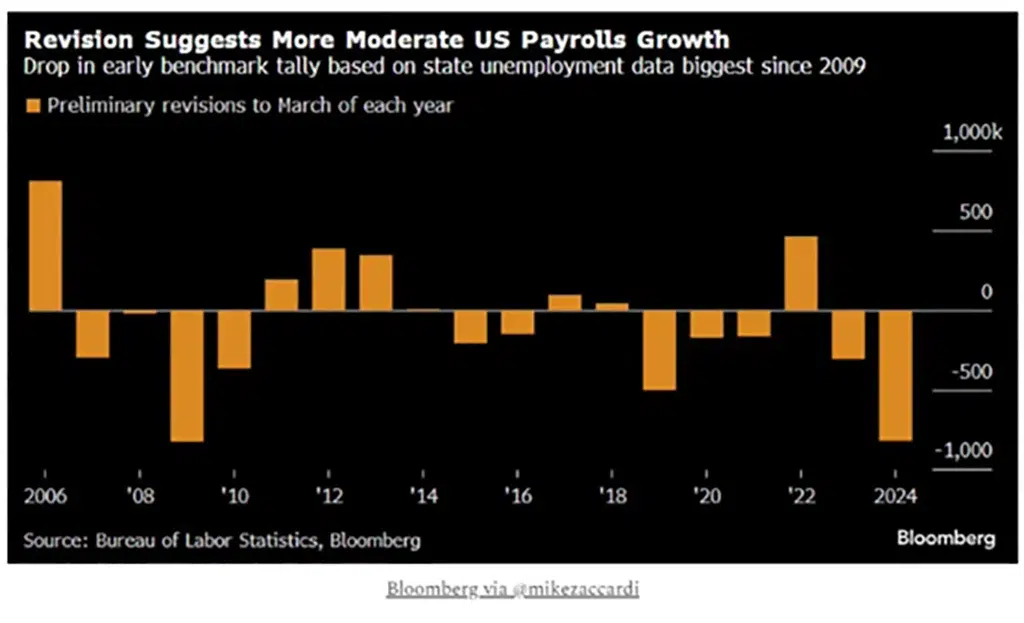

Additionally, this past week, the BLS (Bureau of Labor Statistics) revised job growth for 2024 downward (sharply). Jobless claims also jumped, and suddenly, the labor market looks a bit weaker than expected. See chart below:

BLS revisions. The preliminary revision showed 818k fewer jobs in the year through March than originally estimated. That brings the pace of job growth from 242k to 174k per month.

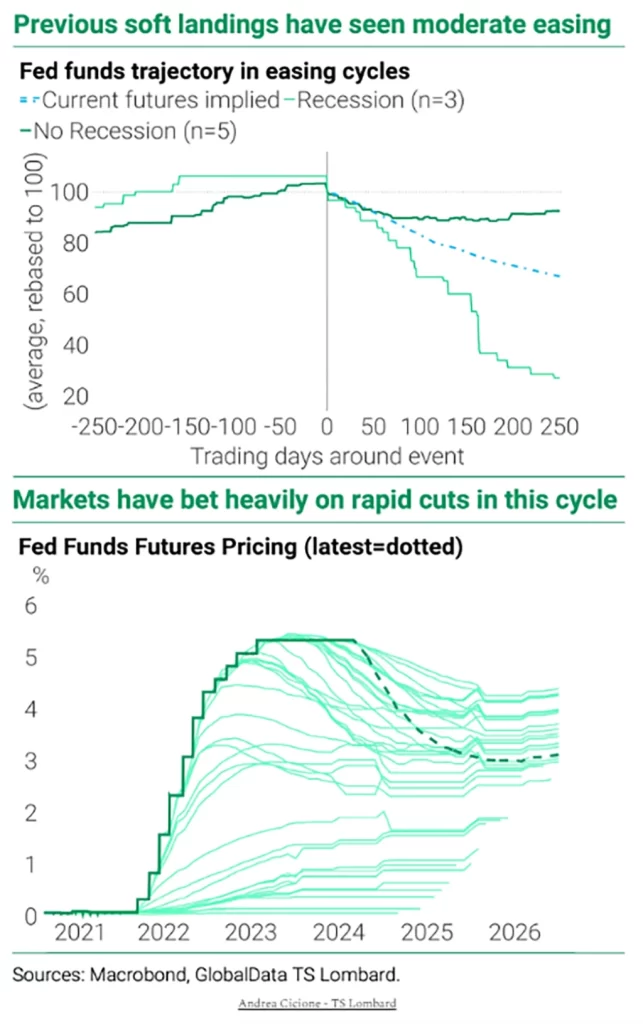

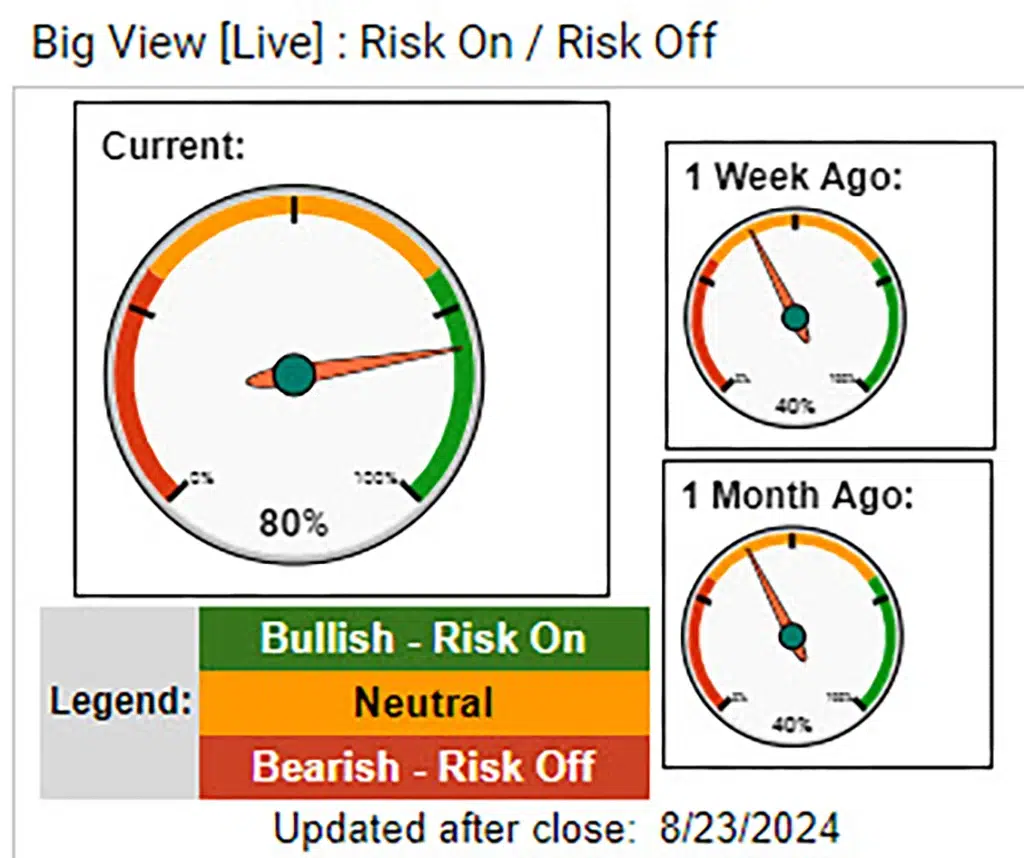

The stock and bond markets have been hanging on the anticipation that the Fed is ready to get more dovish and begin the lowering rate cycle. Odds that are in the futures markets currently show a reduction of 1.0% in the Fed Fund rates by year-end. Personally, with strong earnings, positive GDP and consumers’ still robust spending (see last week’s Market Outlook on retail spending), I wouldn’t take that bet. I would like to see 0.50%-0.75% in a rate reduction. That would be a good start.

Typically, the Fed is gradual in the first rate cuts. However, the markets, as noted above, are expecting an aggressive reduction in rates by year-end, signaling a harder landing than anticipated. See charts below.

Fed vs. market. “Historically, the Fed has been relatively gradual in policy easing during soft landings, which contrasts with current market pricing.”

{kind=link}