Target Investing

The 9 Advantages of This Type of Investing

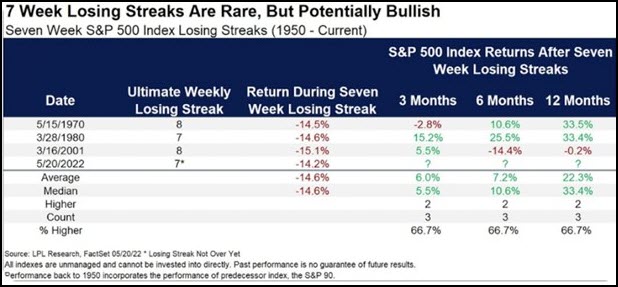

Can you make sense of this?

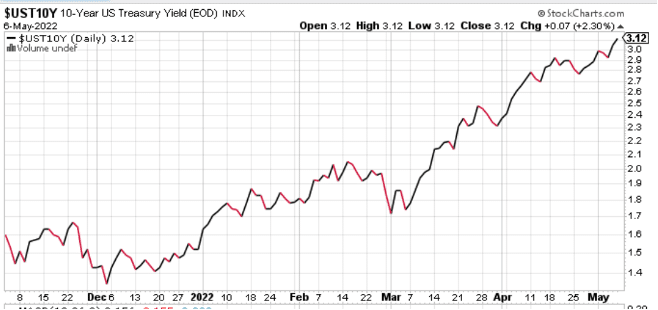

Two weeks ago, the markets experienced a brutal sell-off (S&P 500 down -6.1%) due to inflation rhetoric, rising gas prices, 75 bp Fed Funds rise, and the fastest acceleration of the 10-year US Treasury in history.

Last week the S&P 500 jumped 6.7% and recovered all of the prior week’s losses.

It appears as if all the bear market narratives have all but disappeared. The 10-year interest rates dropped back down to close to 3.0% (from 3.25% the week before), oil fell over 5% (from $120 to $113), and the major banks (JPM) insinuated that we may dodge a recession. The stock market liked this commentary.

Did things change that fast? Did all the world’s problems go away?

We don’t think so.

While the inflation story may have temporarily peaked, it is far from over.

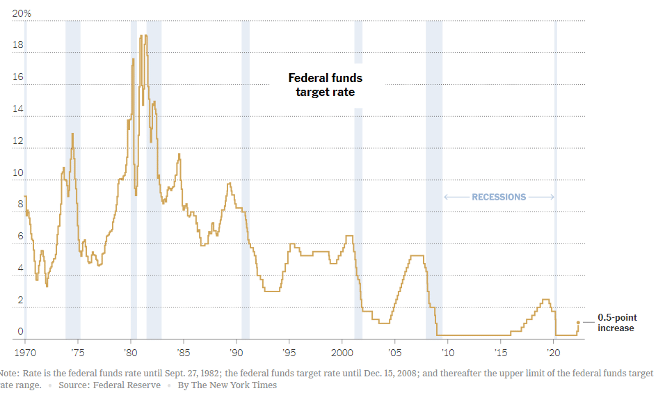

If you look back to the 70’s when we last experienced this type of out-of-control inflation, it took several years and significant interest rate hikes to get it under control. Inflation peaked at 12%, gasoline was in short supply, interest rates peaked at 16%, and stagflation plagued the economy for almost 10 years (1973 to 1982).

It is nearly impossible to believe that inflation has subsided in any meaningful way.

As we have written before, inflation is punishing and insidious. It lasts far longer than anyone expects. In fact, as Mish has pointed out on numerous shows this week, inflation and especially stagflation will be around for many months, if not years. See her explain the severity of the situation in a few of her national media appearances from Friday below.

Cheddar News: Market Wrap Up for a Wild Week

Fox News with Neil Cavuto: With So Many Current Events- What Will the Market Do?

UBS Wealth Management: Volatility and Uncertainty Continue

Friday’s fierce rally was nothing more than a short-term reprieve.

Coincidentally, rallies like Friday’s are even more likely at the end of a quarter because this is when Wall Street and the investment community are rebalancing and repositioning their portfolios.

It’s in Wall Street’s best interest to drive prices up near the end of the quarter to take advantage of fee billing which is based on balances on June 30.

The Inflation Problems Persist

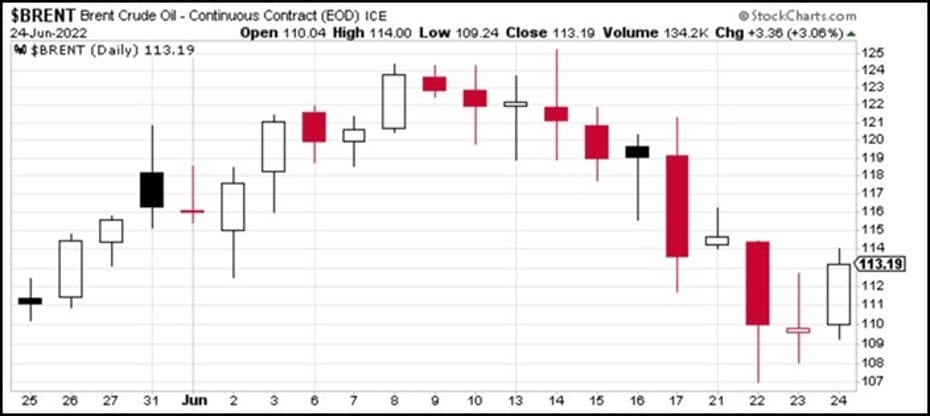

Friday, oil prices (and oil-related stocks) were back up a few dollars and the world began talking, yet again, about the energy supply constraints in Europe that would likely spill over to the US.

In the past month, we’ve seen oil spike to a high of $124 a barrel, come down to $107 and end the week at $113. Gasoline still hovers around $5.00 a gallon nationally. The precious commodity remains volatile and has a short-term impact on interest rates and the broad stock market. (See oil chart from this week below).

The Problem Is Bigger Than Oil

We are starting to hear from a few manufacturers, (it was TESLA this past week), who began whispering about laying off highly compensated employees due to the scarcity of products and the ongoing debacle of the global supply chain.

Even worse, some foods are increasing in scarcity, and we are approaching an important holiday where people will be tested as they’ll have to choose to buy food for the family or gas to get to work or visit family.

The Problem Is Bigger Than Oil

We are starting to hear from a few manufacturers, (it was TESLA this past week), who began whispering about laying off highly compensated employees due to the scarcity of products and the ongoing debacle of the global supply chain.

Even worse, some foods are increasing in scarcity, and we are approaching an important holiday where people will be tested as they’ll have to choose to buy food for the family or gas to get to work or visit family.

We remain in the early innings of a difficult and challenging market. There are just too many factors, including potentially disappointing earnings, that are upon us in the near future to expect anything more than a bear market bounce.

Why Target Investing Is So Important (and Leads To Good Risk Management)

If you watched any of the Mish replays from above, you inevitably heard Mish talk about the current economic environment as a “Trader’s Market.”

Mish’s Premium strategy, and our Algo-based mechanical investment solutions, employ methodical RISK MANAGEMENT. As a result, several of them are positive on the year.

“You can’t hit a target if you don’t know what it is”

- Tony Robbins

“Nobody ever lost money taking a profit”

- Bernard Baruch

Here are a few key takeaways from implementing MarketGauge Target Investing (Risk Management):

Click here to continue reading the 9 advantages from implementing MarketGauge Target Investing and review this week’s text and video market insights from Big View.