Weekly Market Outlook

By Donn Goodman

May 01, 2023

Welcome back to our loyal readers and subscribers. We appreciate that several of you reached out these past few weeks with your comments about our services and the kind things you shared about this weekly column, the Big View bullets, and Keith’s videos. THANK YOU!

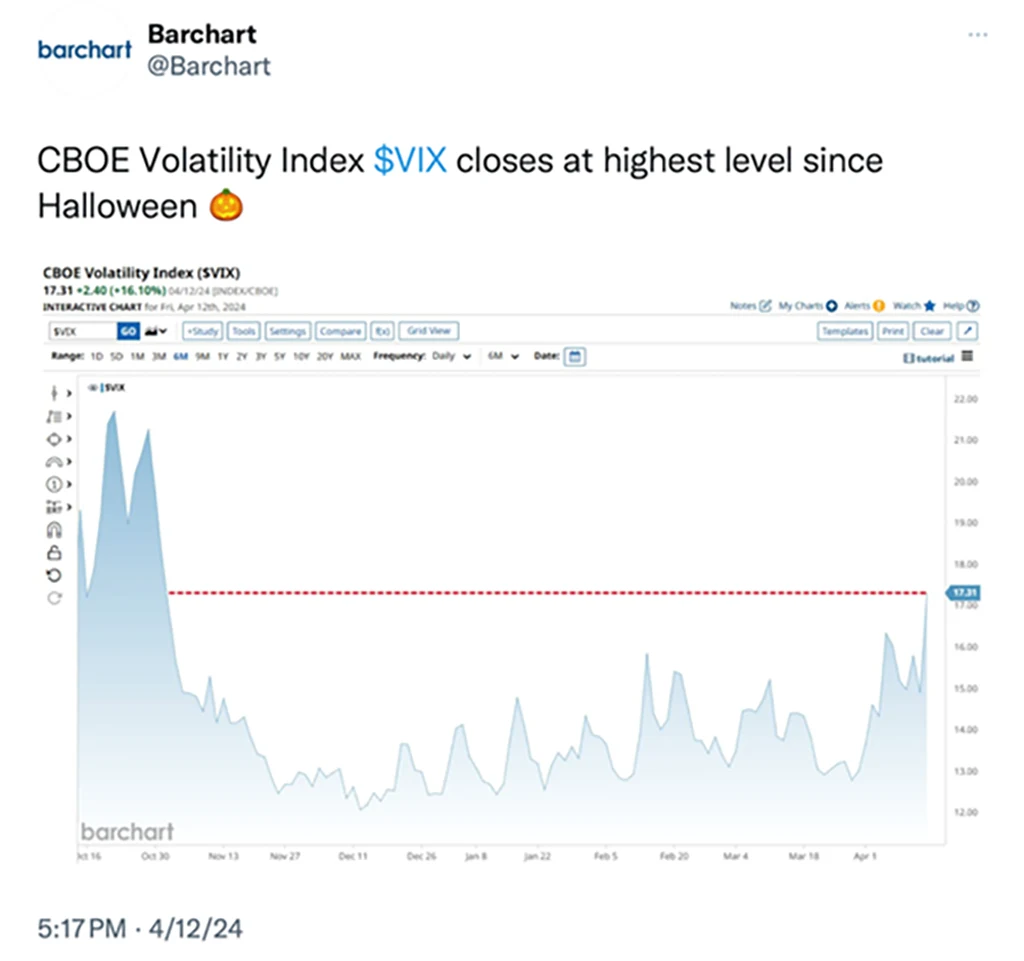

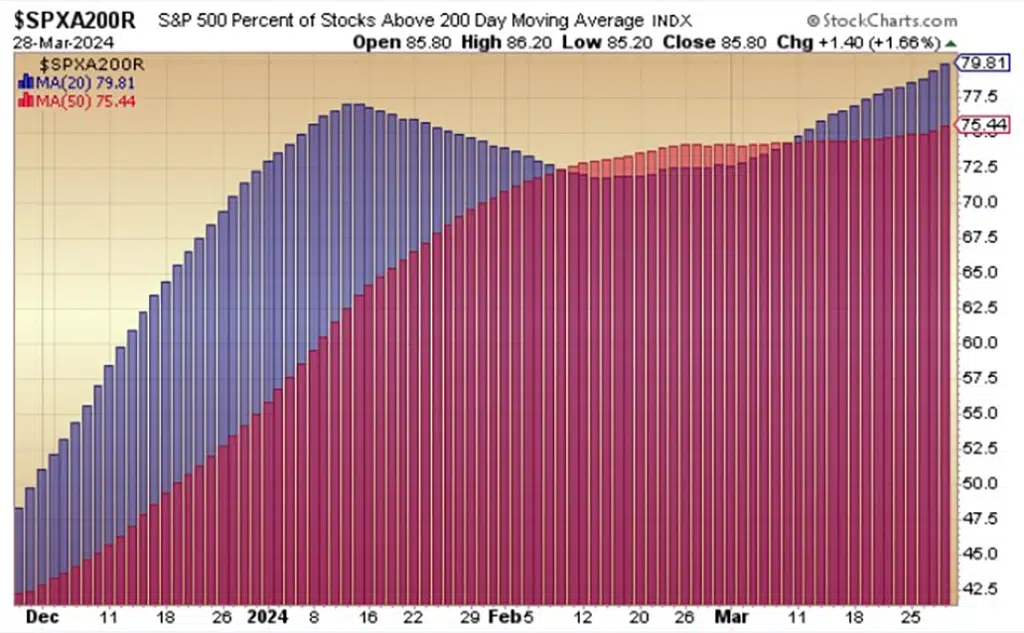

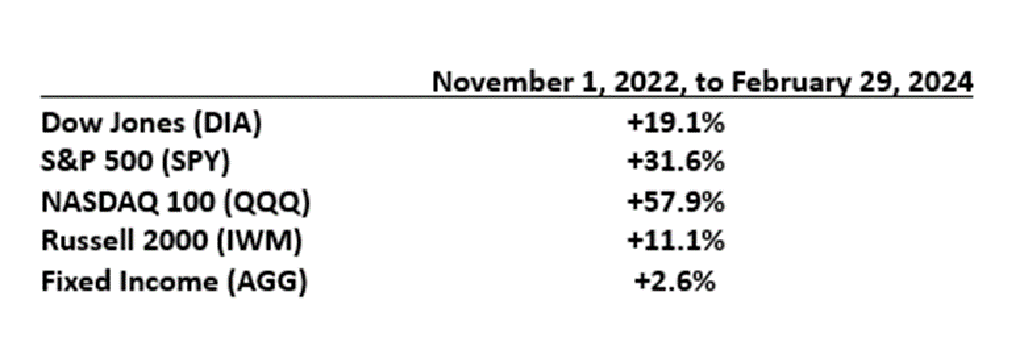

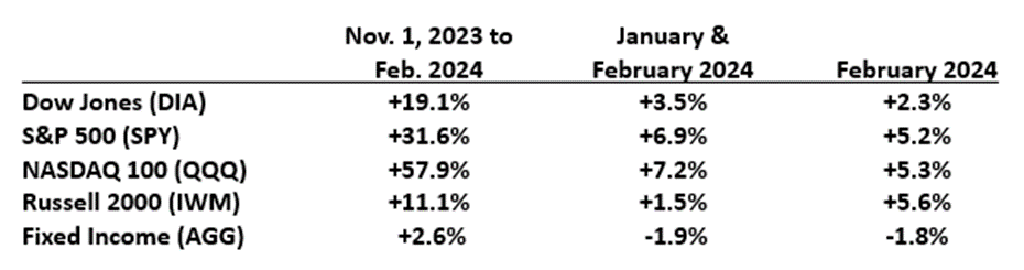

The stock market gyrated this past week, heavily influenced each day on another new (and negative) data point. As you may be well aware, the markets have just gone through a mild two-week pullback, with the NASDAQ and the Dow essentially giving up most of their year-to-date gains. Small and mid-cap stocks are now underwater year-to-date. However, the S&P 500 maintained its positive footing as the positive move in the large mega-cap tech stocks still maintain a 30%+ weighting in the index.

Economic data provides a negative back drop, for now.

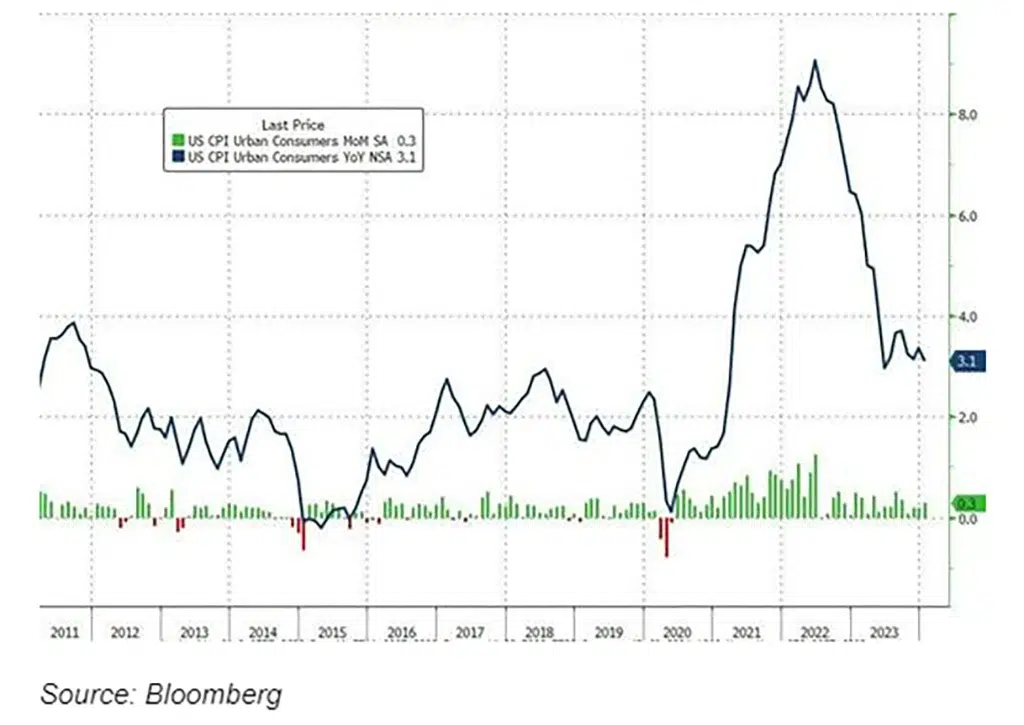

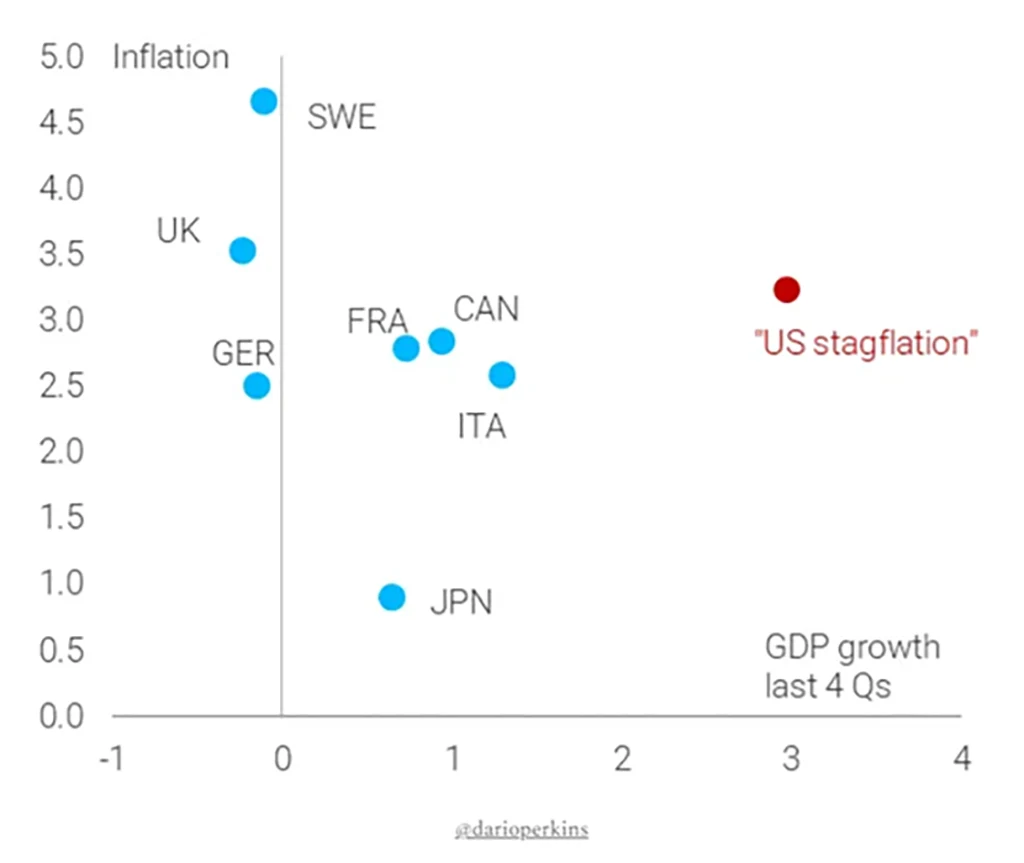

Thursday started out with a tepid GDP report of just 1.6% growth and higher first quarter inflation. This immediately was picked up by investment analysts and news media as the “US Economy has hit STAGFLATION.”

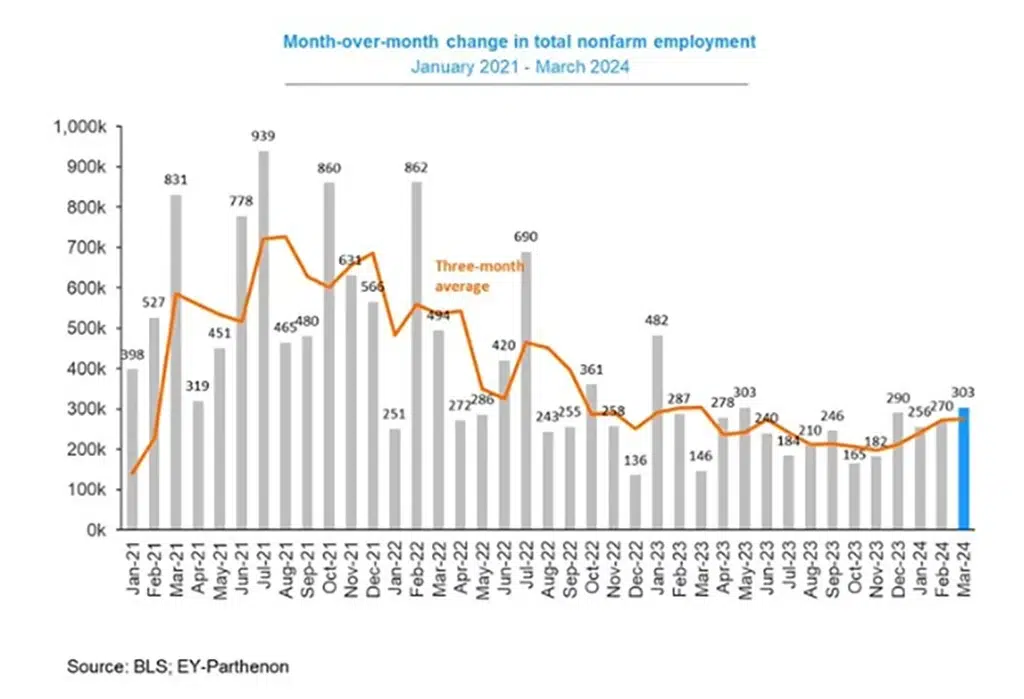

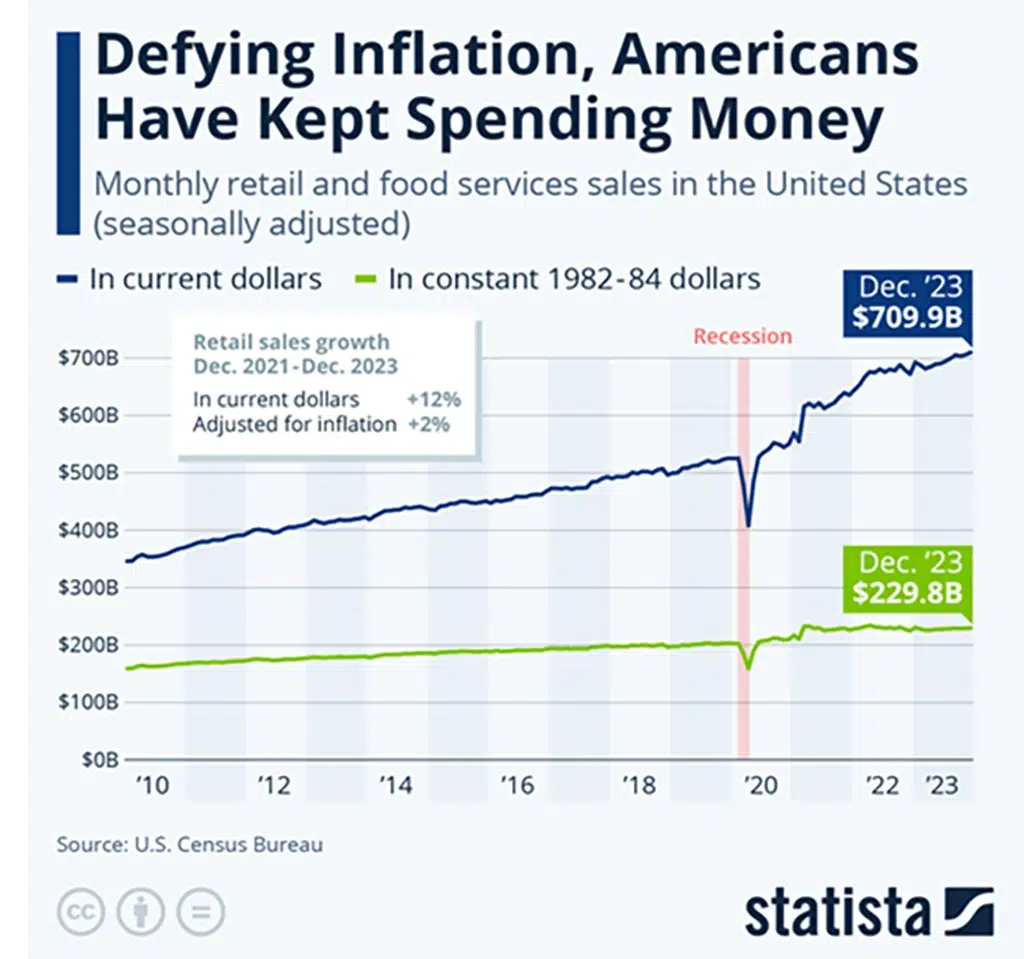

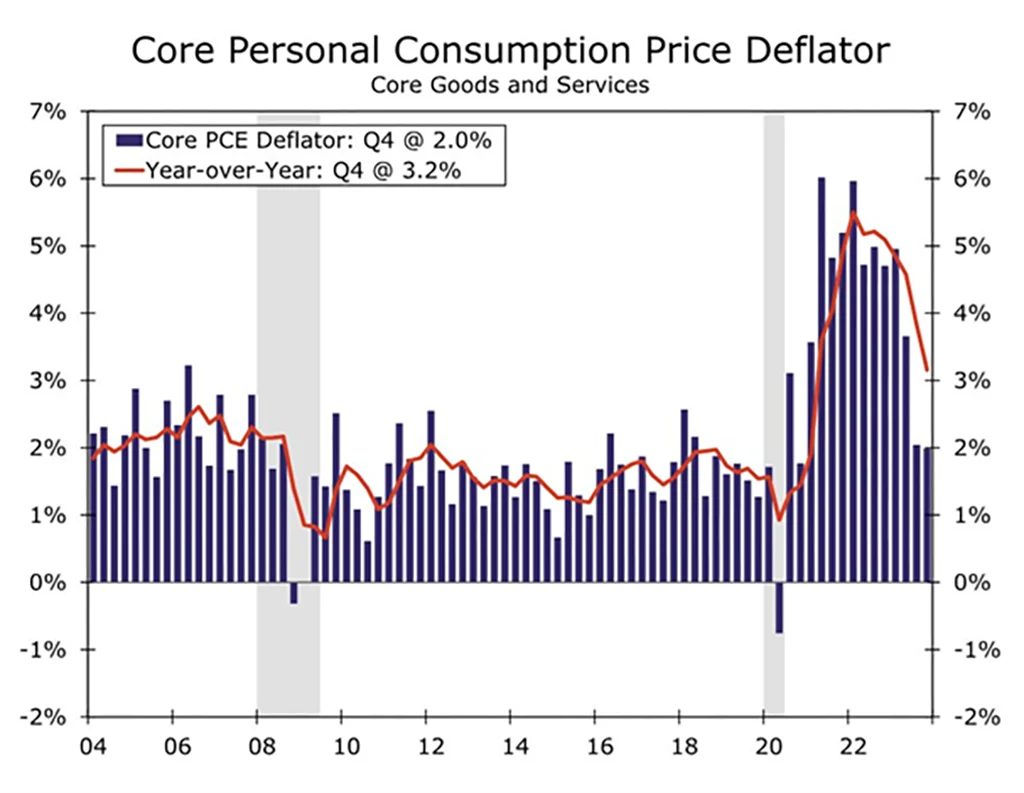

Friday, the core PCE data showed the uptick in inflation, which came out at 2.8% year over year versus the expectations of 2.7%. The biggest driver to this was service inflation of 0.4% for the month of March. Personal spending rose 0.8%, while personal income rose just 0.5% during this period. A big negative to the report was the fact that the personal savings rate fell to 3.2% from 5.2% a year ago. This speaks volumes that the consumer is tapped out, doesn’t have much more to spend to keep up with the inflationary environment, and the GDP report showed a dramatic slowdown in the growth of the economy. (Thanks to Jeffrey Hugh, www.jwhinvestment.com for some of these numbers)

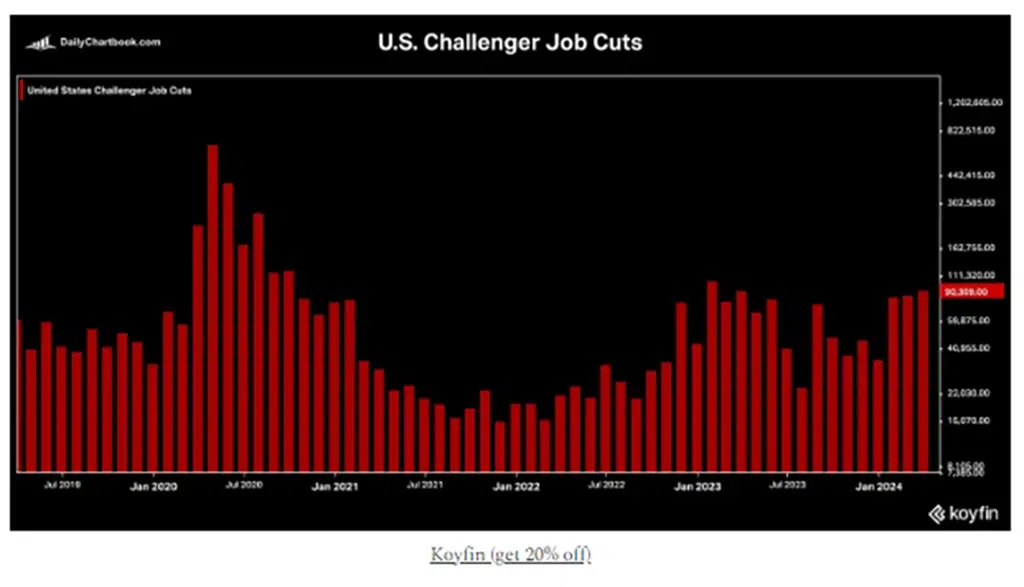

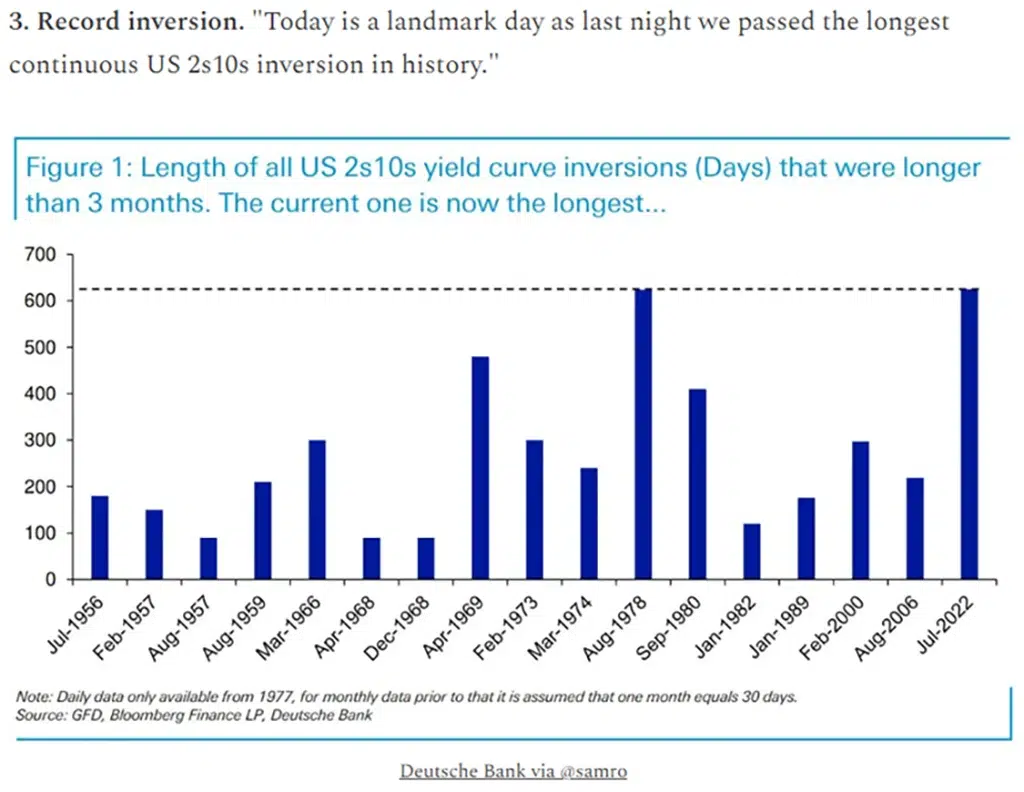

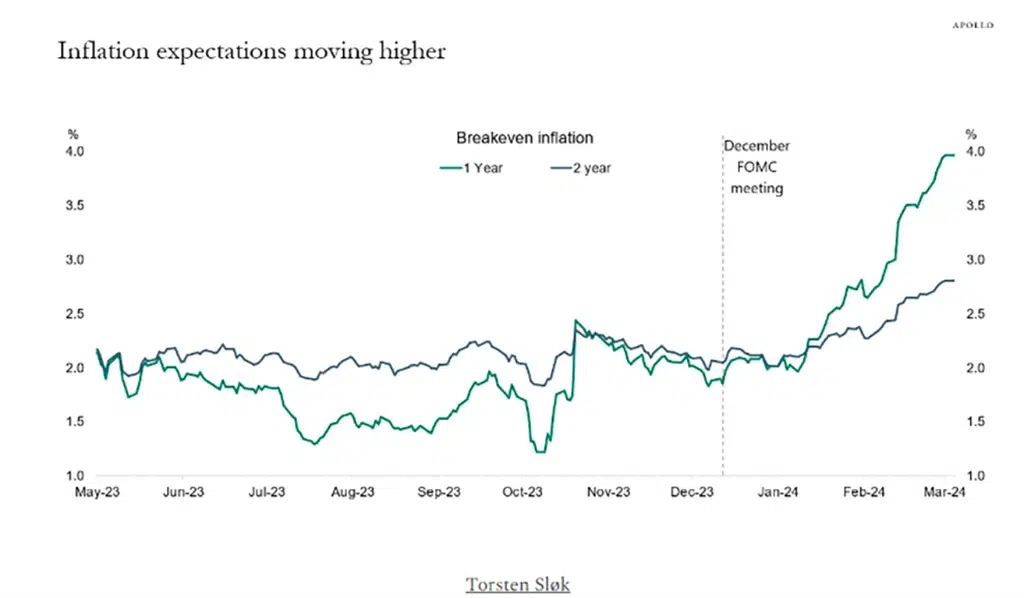

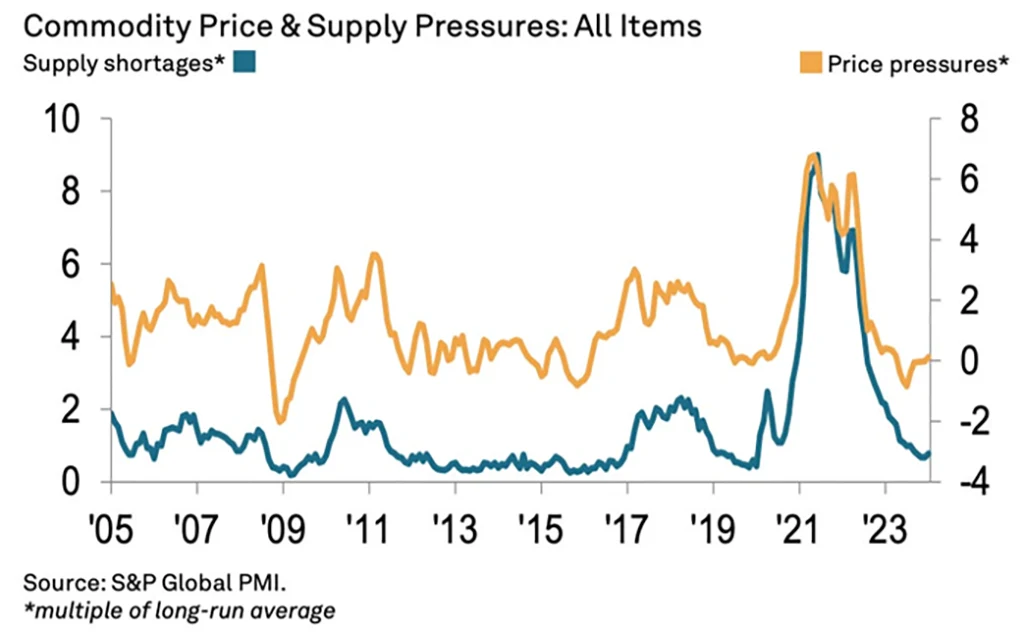

This is humorous to me, given that Mish has been on National TV shows, like Fox with Charles Payne, as far back as 9-12 months ago, suggesting STAGFLATION was coming. Low growth and persistent inflation. Now it seems every analyst and talking head utters this word (STAGFLATION) once a day. Additionally, this word can be heard in other parts of the world as many developed countries’ economic backdrops look similar to those of the US: slow growth and elevated inflation. See chart below:

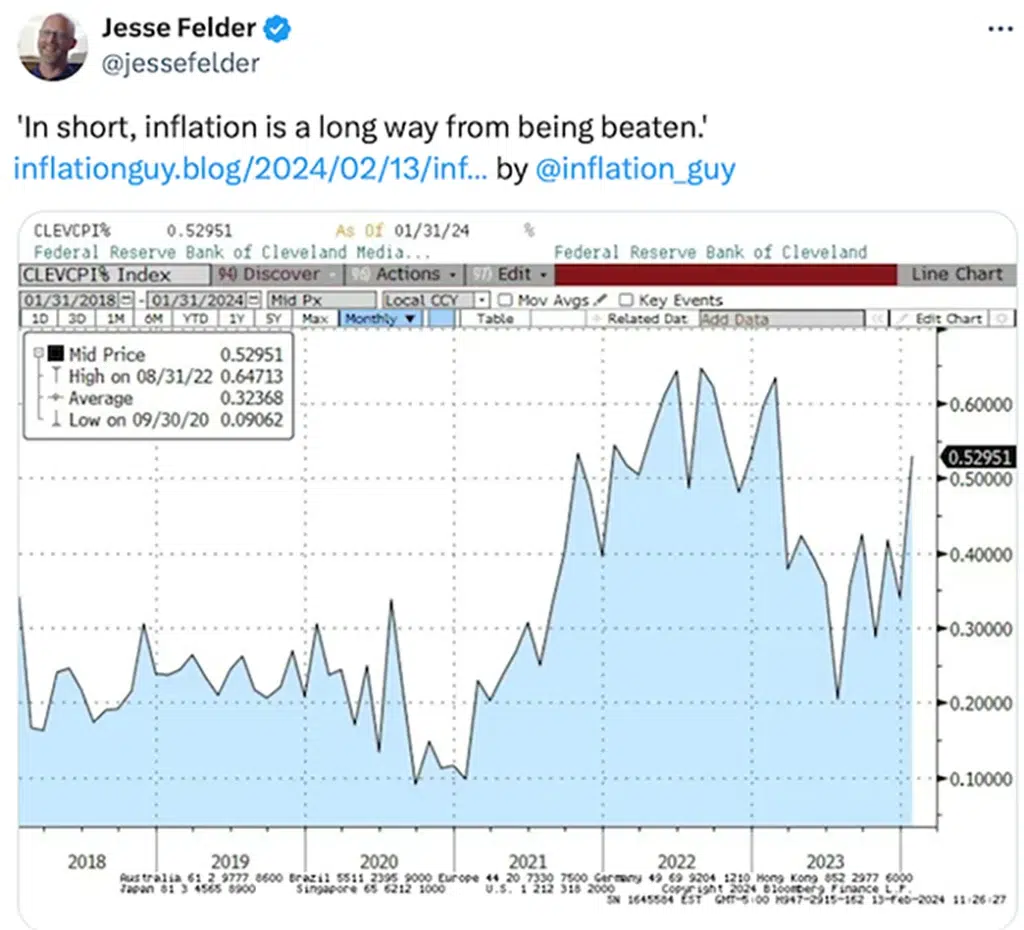

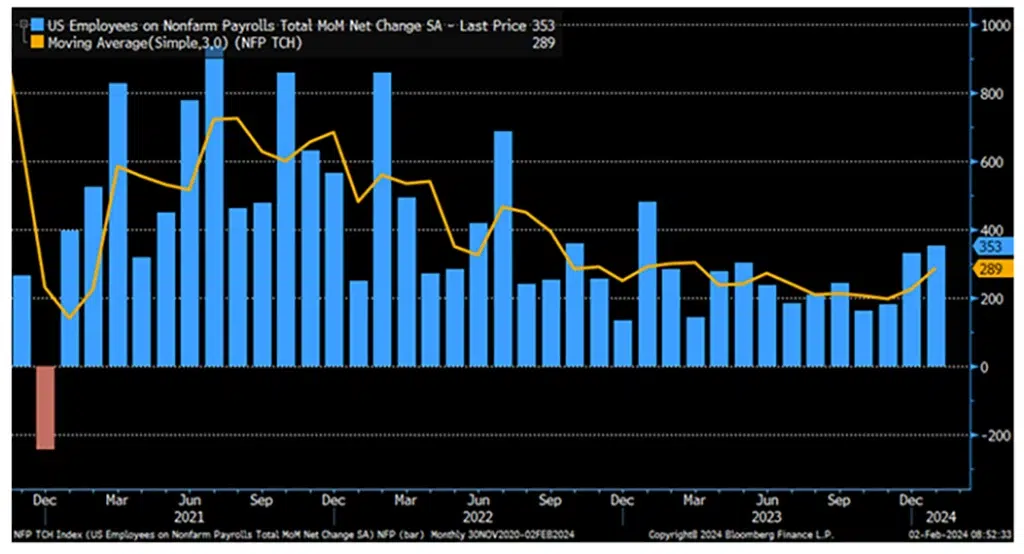

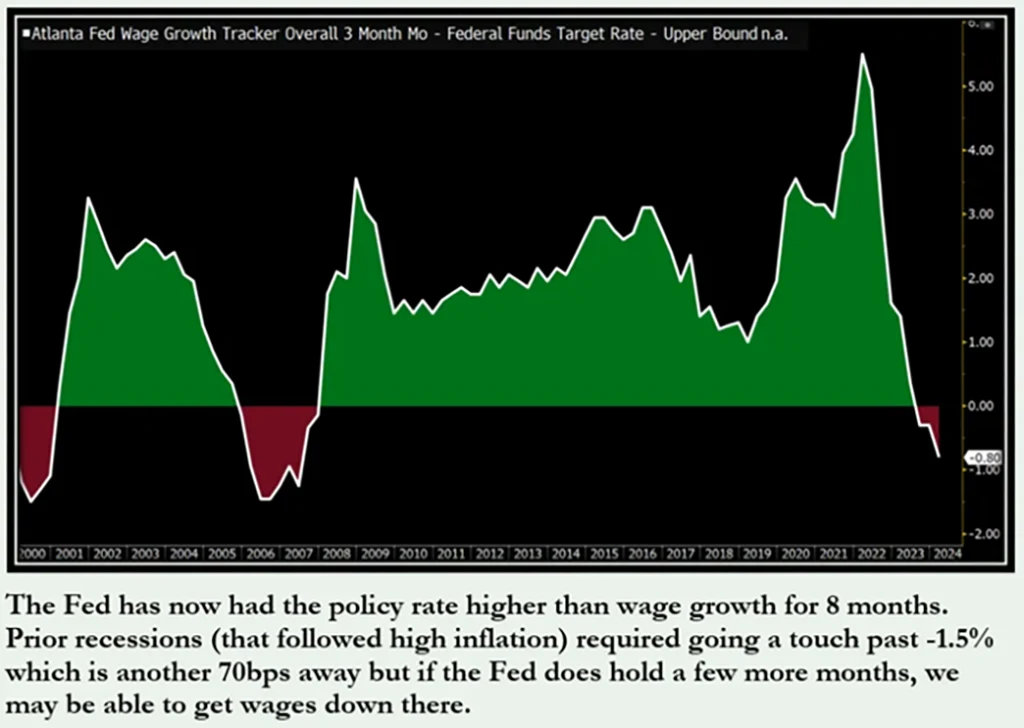

Wage growth is also slowing (not helping), which could reduce the savings rate and GDP in the near-term. See chart below:

Don't Get The Weekly Newsletter? Join Here:

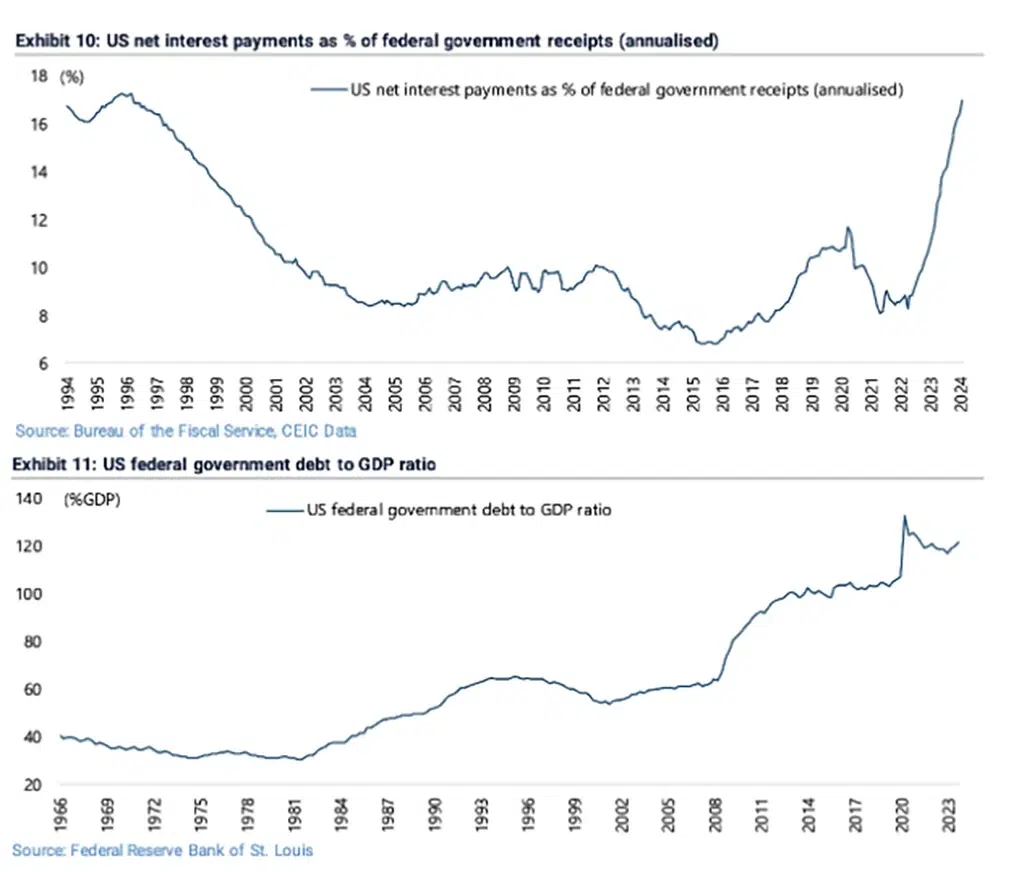

If one were to strip out government spending the past year ($6.8 trillion deficit in the past 12 months), one would see that we are actually in a negative GDP environment except for government spending.

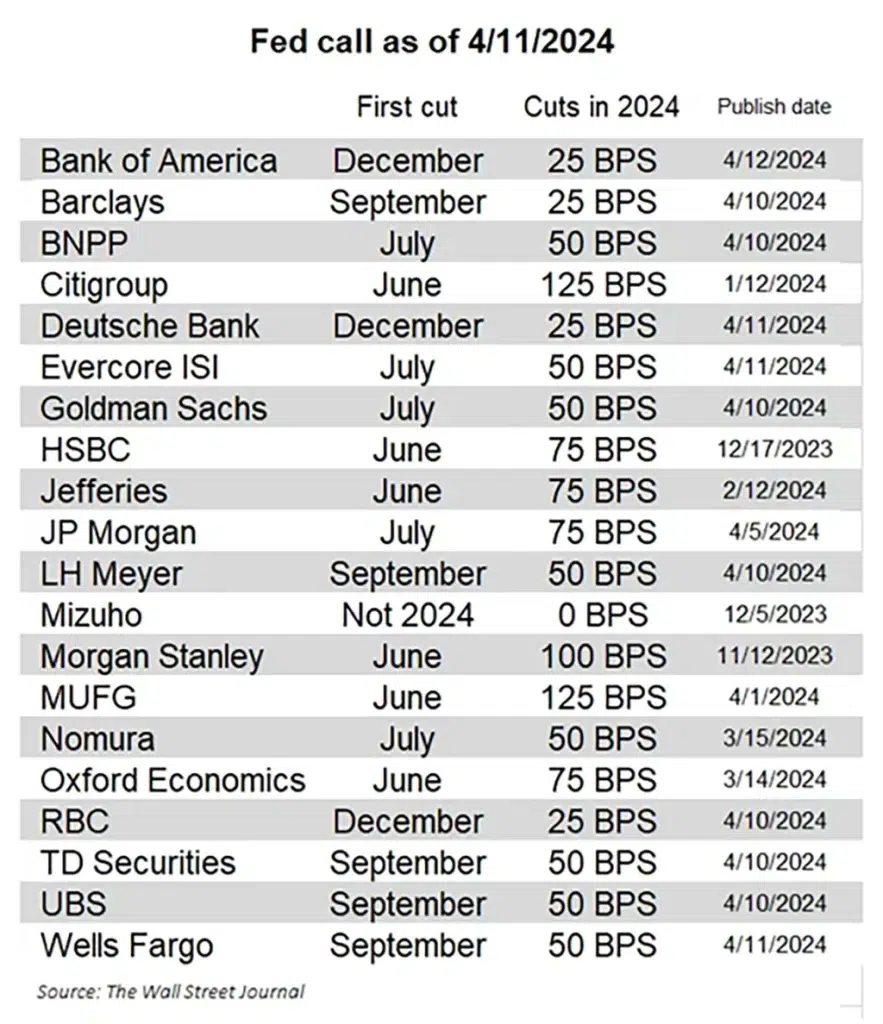

We have stated on the record frequently in this weekly commentary (and Mish has stated on social media as well as the TV airways) that we saw interest rates staying higher for longer.

We also want to be clear that earlier this year we suggested that there would be NO interest rate cuts by the FED until later on in 2024. In fact, we have alluded to the fact that the FED should consider hiking interest rates instead of cutting them.

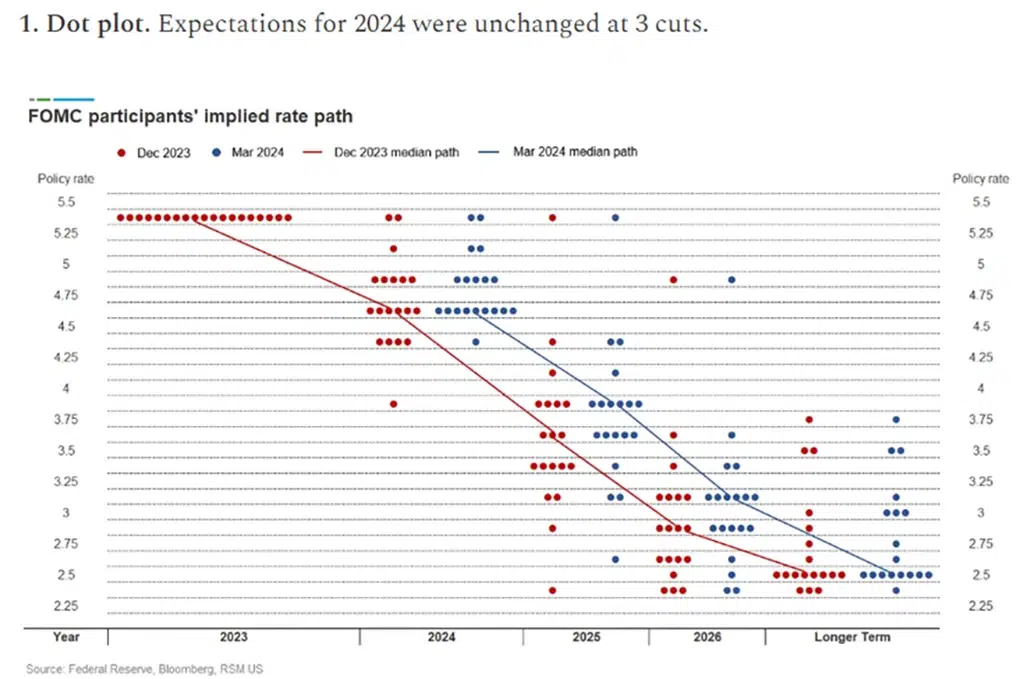

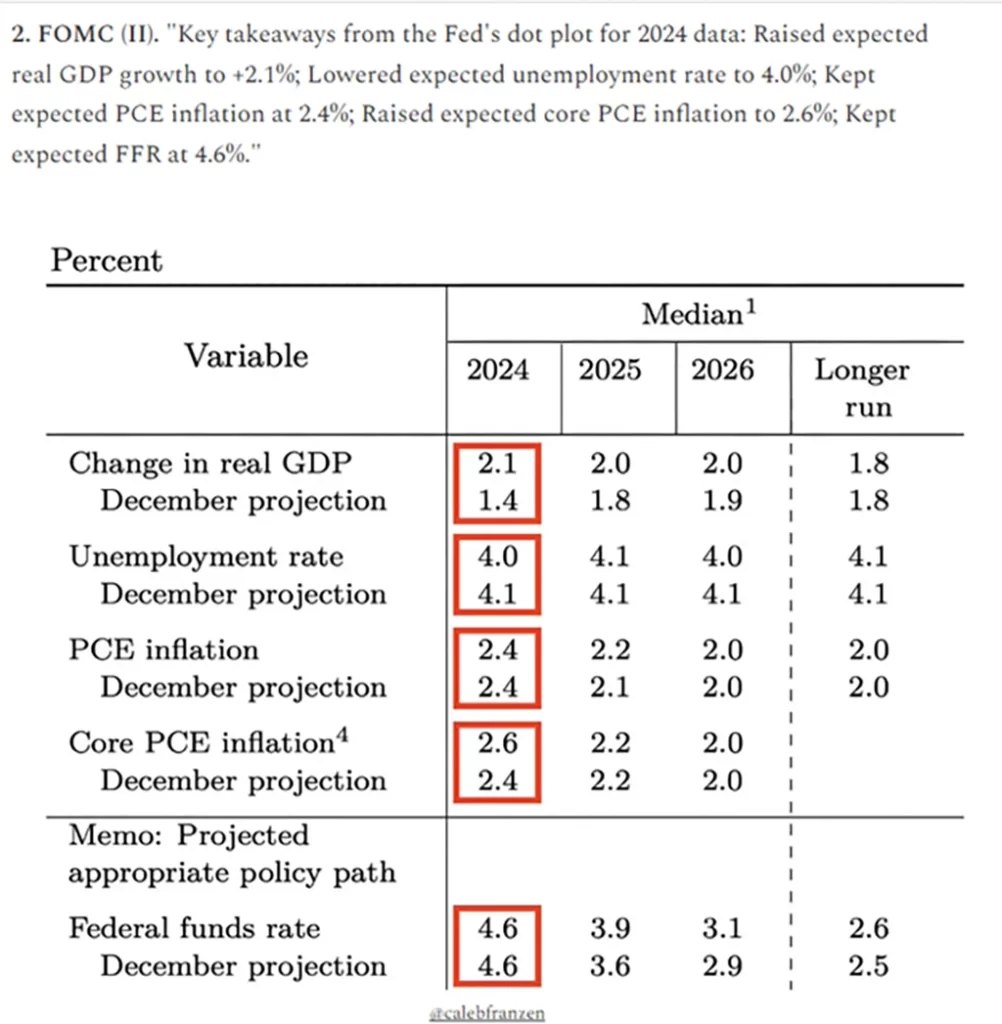

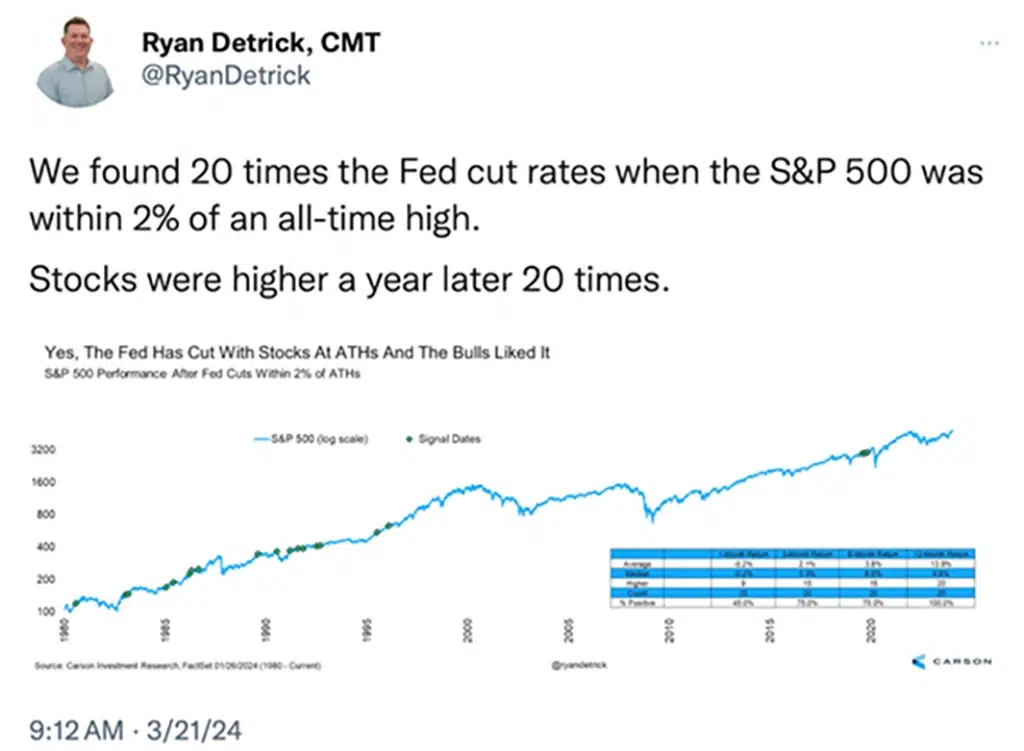

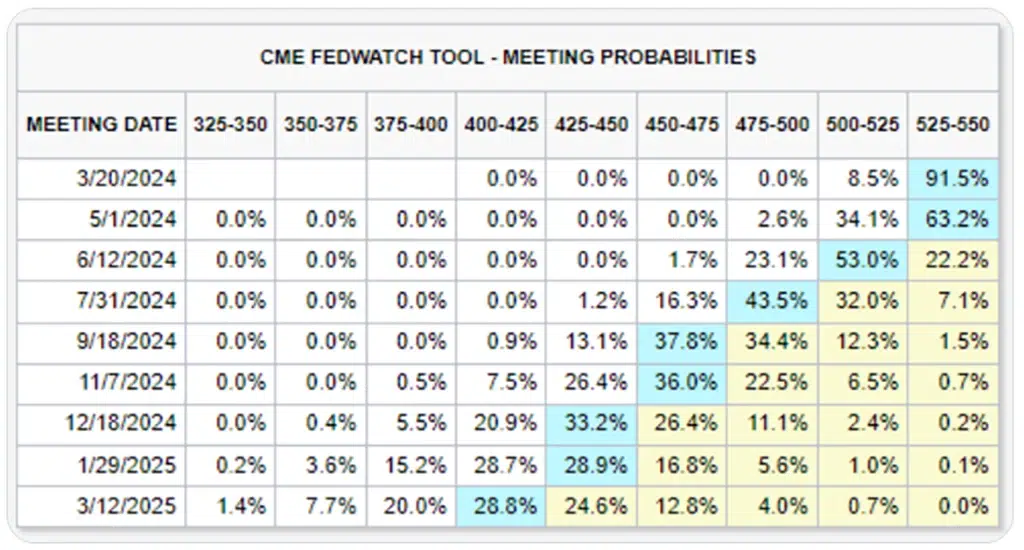

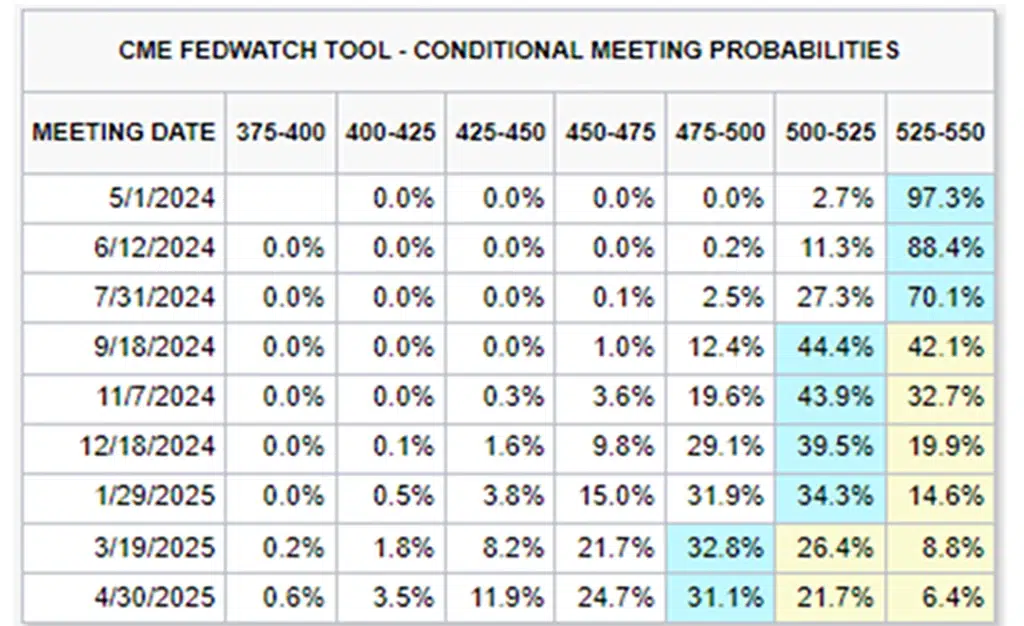

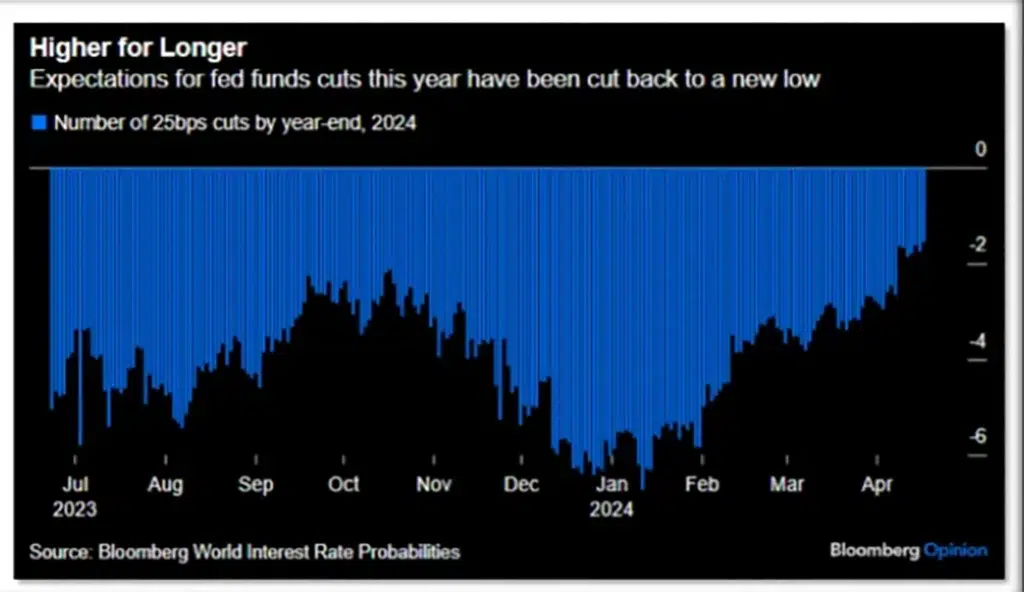

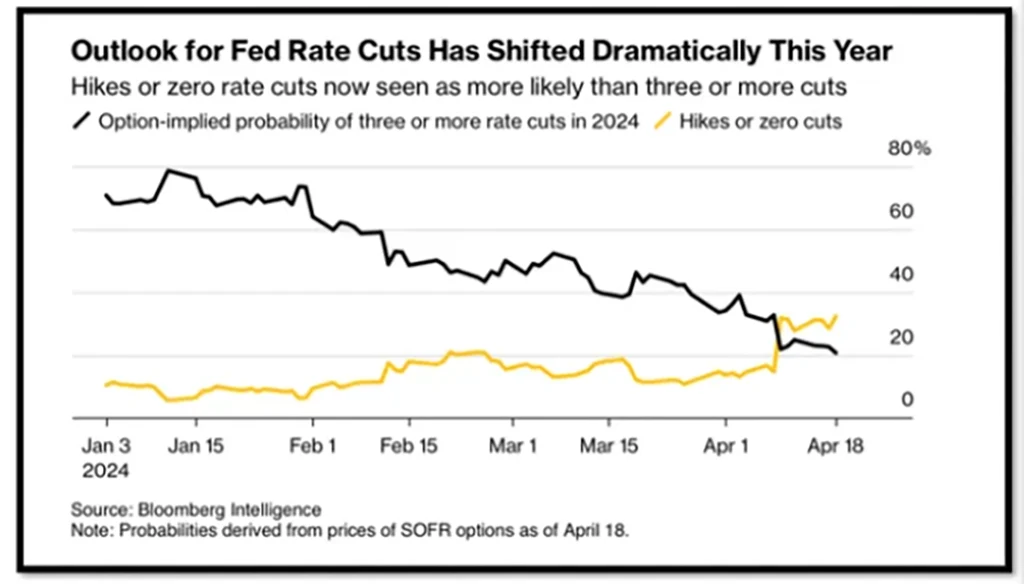

This week, the odds shifted dramatically from cutting rates at the June meeting to probably not cutting until later in the year, if at all. Some expectations have also shifted to odds improving for another hike. See the charts indicating this below: (Odds have shifted to no cuts until possibly September).

To us, it is a fact that the longer rates remain elevated, the greater the effect this restrictive monetary policy may have on the economy. This may result in the US economy slipping into a recession. If the market gets wind of this and breaks down then it would be highly likely the FED would cut rates to repair the damage done by a negative stock market and stifling economy. That is how it could play out.

As we mentioned above, we could even see the Fed hike rates one more time if they feel that the recent uptick in inflation is too much. See the charts below showing how dramatic the Fed’s position has changed these past few months:

On the bright side.

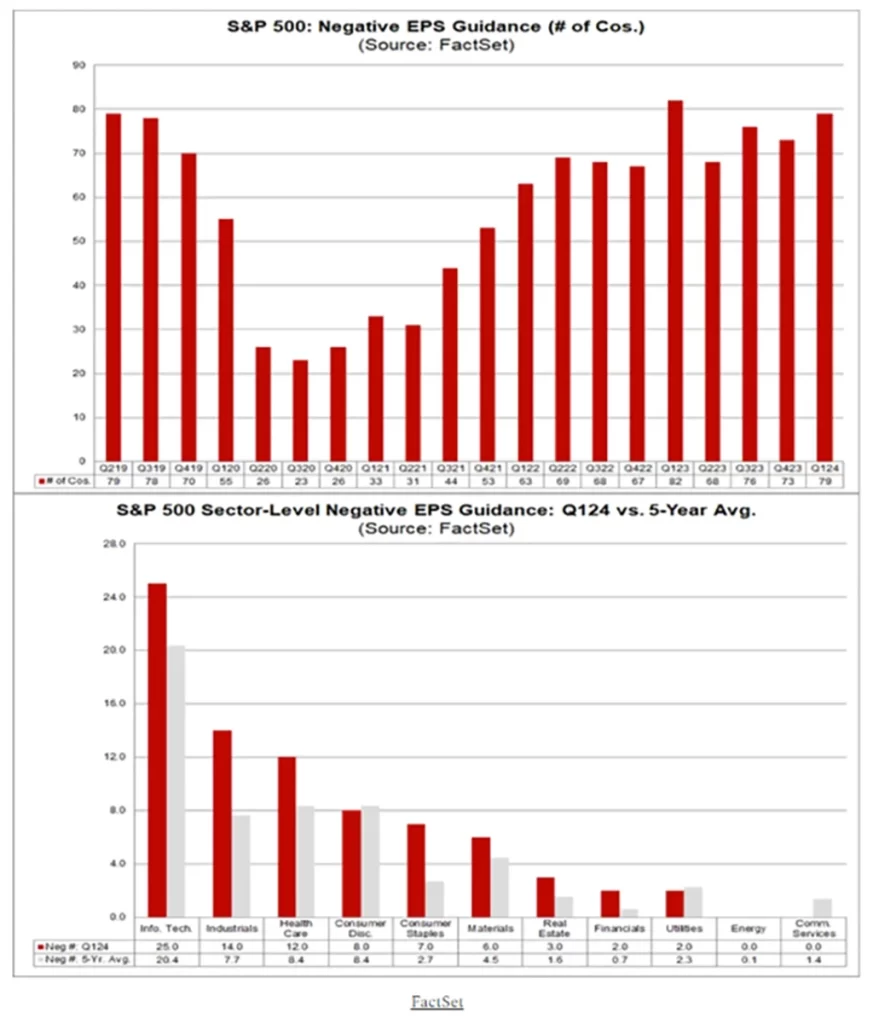

We are in earnings season and many of the companies that have reported so far have exceeded expectations. According to FactSet, 46% of S&P 500 companies have now reported their Q1 2024 results with 77% beating their earnings estimates and 60% reporting revenues above estimates.

These are good numbers so far and these earnings expectations may very well hold up the markets while interest rates stay high with inflation remaining elevated and sticky..

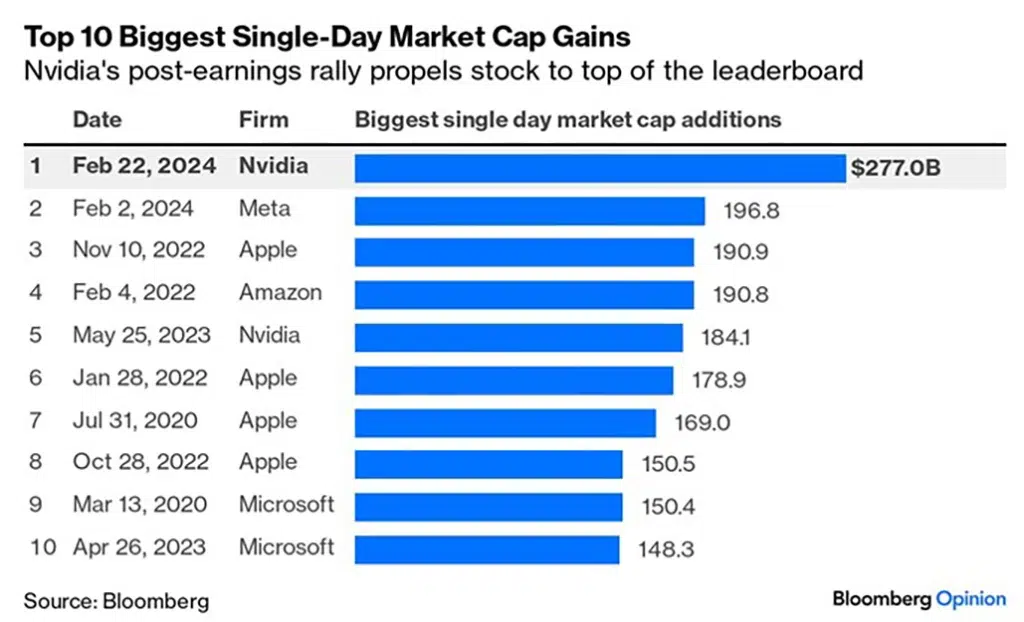

Such was the case this past week with three of the Magnificent Seven stocks. Meta (Facebook), Microsoft and Google all beat their expectations. Meta was down more than 10% after reporting a negative outlook for Q2. Microsoft and Google blew away earnings. These three companies (META, MSFT, and GOOG) all stated the same narrative during their earnings calls. They are upping their AI cap ex dramatically, and that helped MU, SMCI, and NVDA all have a BIG UP day on Friday as investors now more fully understand the semiconductor companies involved in AI are the biggest beneficiaries of this cap-ex spending cycle.

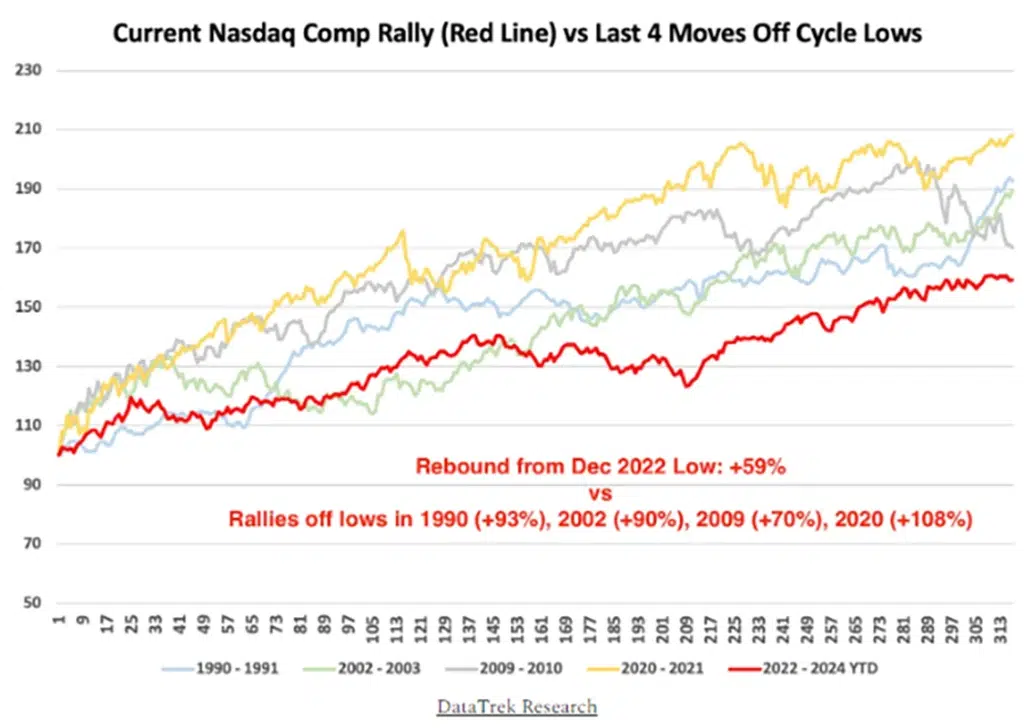

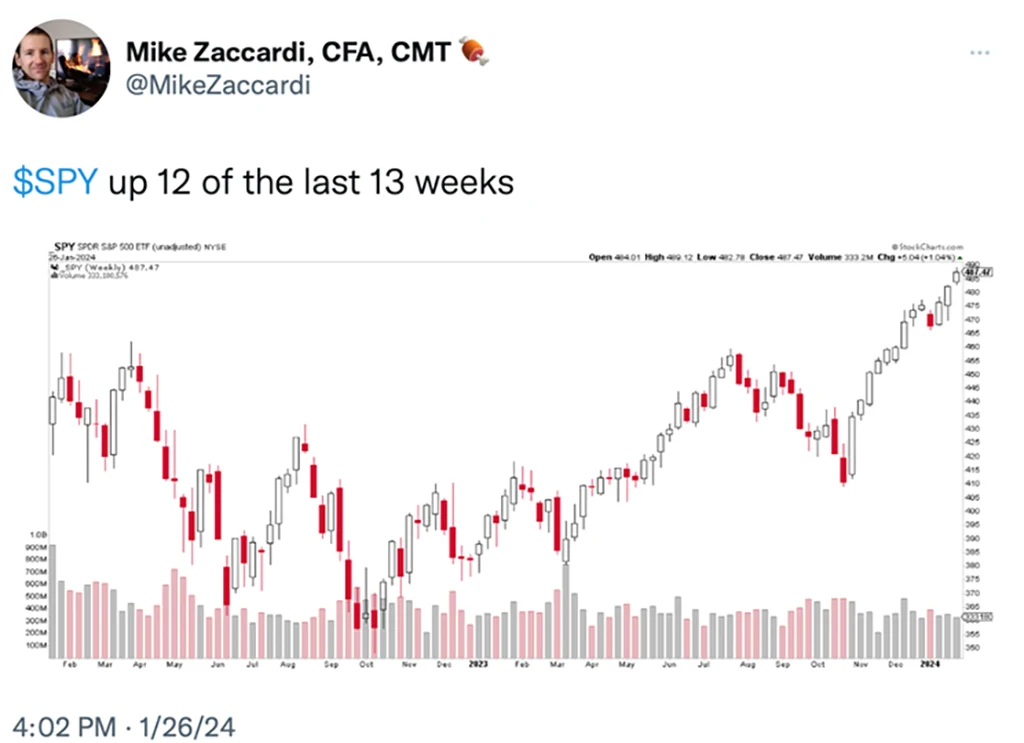

The NASDAQ was up 1.7% on Friday and 3.6% on the week. Semiconductor stocks, which were down over 9% last week regained their upward bias and were up over 9% this past week. See chart below:

Use the link below to continue reading about:

- The brighter side of the market’s condition

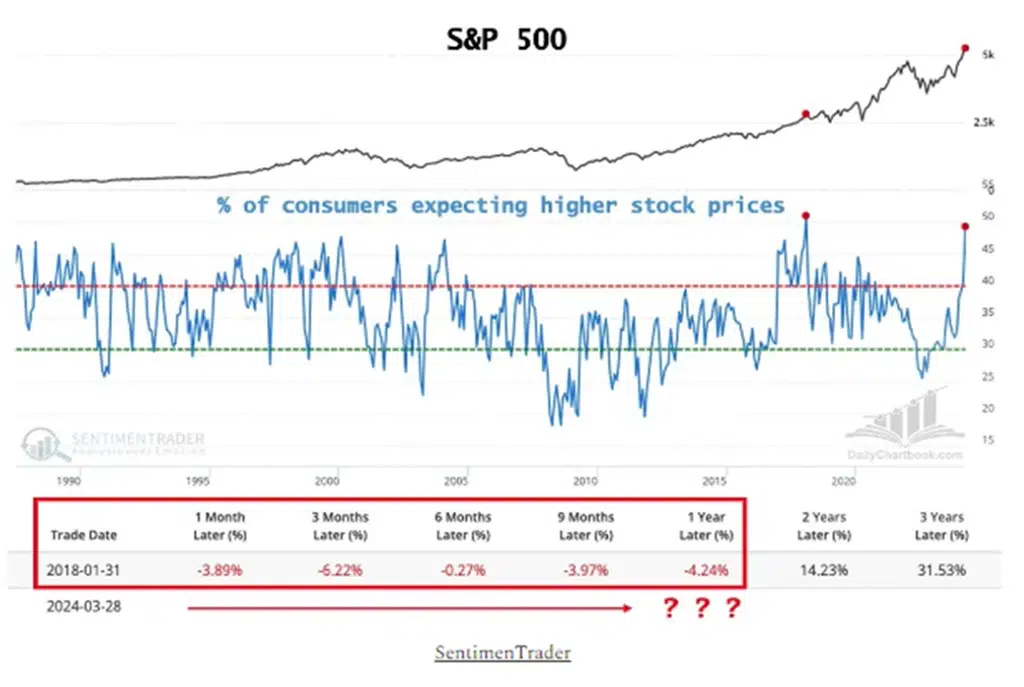

- Statistical outcomes for the rest of the year based on current trends

- Investor sentiment and positioning

- The Big View bullets

- Keith’s weekly video analysis

- And more